Increasing your credit limit lowers your credit utilization ratio. If your spending habits stay the same, you could boost your credit score if you continue to make your monthly payments on time. But if you drastically increase your spending with your increased credit limit, you could hurt your credit score.

Does a higher credit limit improve your credit score?

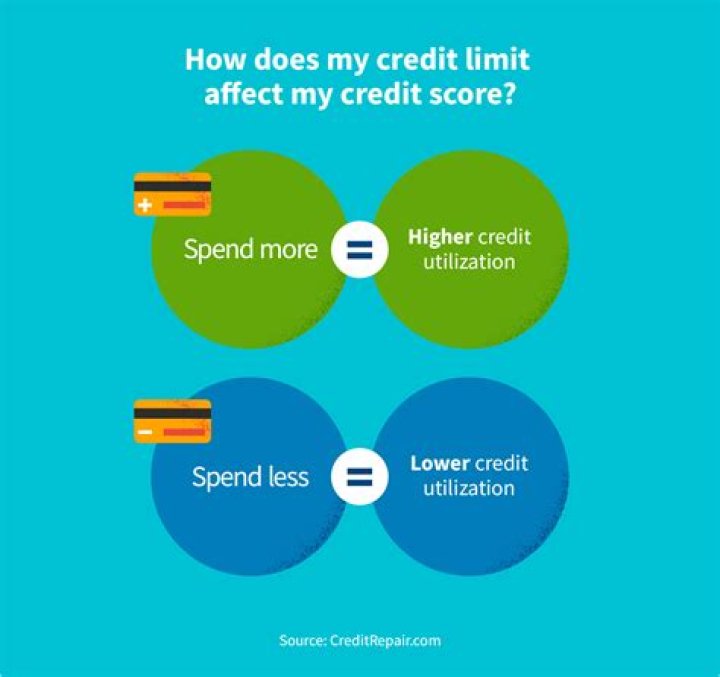

Increasing your credit limit can lower credit utilization, potentially boosting your credit score. A credit score is an important metric lenders use to determine a borrower's ability to repay. A higher credit limit can also be an efficient way to make large purchases and provide a source of emergency funds.Does credit limit affect credit score?

Although a credit limit increase is generally good for your credit, requesting one could temporarily ding your score. That's because credit card issuers will sometimes perform a hard pull on your credit to verify you meet their standards for the higher limit.Is too high credit limit bad?

Can Too Much Available Credit Hurt Your Score? There's no such thing as too much available credit when it comes to your credit score. As the data suggests, people with exceptional credit use only a small fraction of what they have on their credit cards, and that has helped their credit scores.Is 7000 A good credit limit?

A high-limit credit card typically comes with a credit line between $5,000 to $10,000 (and some even go beyond $10,000). You're more likely to have a higher credit limit if you have good or excellent credit.Does Requesting a Credit Limit Increase Hurt Your Score?

What is a good credit limit to have?

Generally speaking, experts suggest keeping your credit utilization below 30 percent for the best results, which would mean having balances of $3,000 or below for every $10,000 in available credit you have.Is it better to pay off your credit card or keep a balance?

It's better to pay off your credit card than to keep a balance. It's best to pay a credit card balance in full because credit card companies charge interest when you don't pay your bill in full every month.How can I raise my credit score to 800?

How to Get an 800 Credit Score

- Pay Your Bills on Time, Every Time. Perhaps the best way to show lenders you're a responsible borrower is to pay your bills on time. ...

- Keep Your Credit Card Balances Low. ...

- Be Mindful of Your Credit History. ...

- Improve Your Credit Mix. ...

- Review Your Credit Reports.

Is there any drawbacks to increase credit limit?

It could lead to more debt: Getting approved for a larger credit line does mean more spending power, but it could also mean getting deeper into debt. If you have the ability to spend more, you just might spend more than you can afford to pay off, thus racking up interest charges.Is 750 a good credit score to buy a house?

A 750 credit score generally falls into the “excellent” range, which shows lenders that you're a very dependable borrower. People with credit scores within this range tend to qualify for loans and secure the best mortgage rates. A 750 credit score could help you: Qualify for a mortgage.Is a 750 FICO score good?

Your FICO® Score falls within a range, from 740 to 799, that may be considered Very Good. A 750 FICO® Score is above the average credit score. Borrowers with scores in the Very Good range typically qualify for lenders' better interest rates and product offers.Is 900 a good credit score?

The best-known range of FICO scores is 300 to 850. Anything above 670 is generally considered to be good. FICO also offers industry-specific FICO scores, such as for credit cards or auto loans, which can range from 250 to 900.Is having zero balance on credit card good?

A zero balance on one credit card won't hurt your credit score and can actually help it by lowering your debt-to-credit ratio. Also known as a credit utilization rate, this factor can have a significant impact on your credit score and experts recommend keeping it below 30% across all your loan products.What happens if I max out my credit card but pay in full?

More videos on YouTubeIf you can max out a card and pay the full balance off on or before your next bill due date, your ratio won't be affected. That's because a credit card issuer only reports your information to the major credit bureaus once a month.