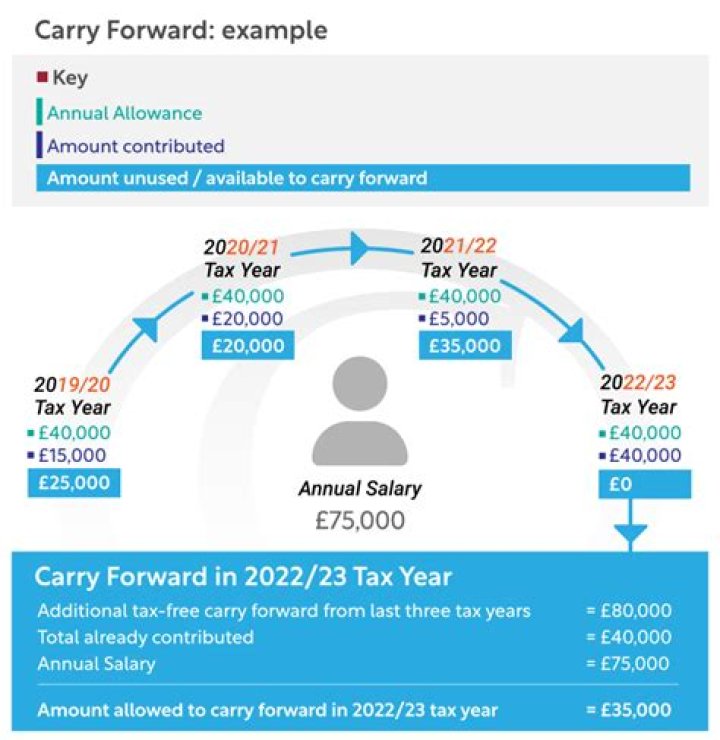

In order to carry forward unused annual allowance from an earlier tax year you must have been a member of any registered pension scheme in that tax year. Annual allowance can be carried forward from the three tax years immediately before the tax year in which you are paying your contribution.

Can you carry forward pension allowance?

You can carry forward unused allowance from the 3 previous tax years. This annual allowance only applies to pension savings made to your UK registered pension schemes, or to overseas schemes where either you or your employer qualifies for UK tax relief.

How many times can you use pension carry forward?

4. You must use any unused annual allowance from the earliest year first (you can only go back three years) and can only use it once. This means it can only be used once and if fully used for a previous tax year, cannot be used a second time.

Can you backdate SIPP contributions?

SIPP backdated contributions This option allows you to make a one-time SIPP deposit of more than £40,000, if you paid less than your annual SIPP allowance in any of the last three years. The following conditions apply: You’ve deposited the maximum amount of £40,000 in your SIPP this year.

What is the maximum you can put in a SIPP?

The amount you can pay into any pension including a SIPP and benefit from tax relief is based on your earnings and how much tax you pay. The general rule is that you can contribute up to 100 per cent of your earnings, with tax relief applying on contributions of up to £40,000 per tax year.

What happens to my SIPP when I die?

When you die, the remaining value of your pension (SIPP) can be passed on to your nominated beneficiaries. The death benefits can either be paid to your beneficiaries as a lump sum or used as an ongoing pension to provide an income and benefit from leaving the money invested in a tax efficient wrapper.

How much can you hold in a SIPP?

You can typically put up to 100% of your annual salary into your SIPP (if you want to)

You must use any unused annual allowance from the earliest year first (you can only go back three years) and can only use it once. This means it can only be used once and if fully used for a previous tax year, cannot be used a second time.

How do I use pension carry forward?

Who can use pension carry forward?

- You had a pension in each year you wish to carry forward from, whether or not you made a contribution (the State Pension doesn’t count).

- You have earnings of at least the total amount you are contributing this tax year. Alternatively, your employer could contribute to your pension.

How much can you transfer into a SIPP?

Your employer can make contributions to your SIPP, as well as or instead of a workplace pension. These contributions count towards your annual allowance, but are not limited by your income. If you do not have any earnings in the tax year, you can still contribute up to £3,600 gross into your SIPP.

When to use carry forward allowance for SIPP?

If you earn more than £40k then carry forward can be used to allow contributions above £40k based on what was contributed in earlier years, so the whole of the current year allowance is usd up, then the oldest of the years available for carry forward.

How can I carry forward unused annual pension allowances?

You can carry forward unused tax relief on pension contributions provided: 1 You are a member of a qualifying pension scheme 2 You have used up your annual allowance for the current tax year 3 You have had qualifying income in each of the last 3 years or if not the carry forward relief will be restricted to £3,600 in any tax year

Do you get tax relief on pension carry forward?

If there were no earnings in any of the years in question they can still contribute £3,600 gross into a pension and get tax relief. How does pension carry forward work? Pension carry forward rules allow an individual to carry forward any unused annual allowance from the three previous tax years and still receive tax relief on their contributions.

How much is the employer contribution to SIPP?

So employer pension contribution increases one’s gross salary for SIPP purposes. £45,000+6% (employer contribution)=£47,700 is the gross salary for SIPP purposes, meaning that the total annual SIPP allowance of £40K can potentially be utilised by topping SIPP for £40K-20% (tax relief that will be claimed from HMRC)= £32,000.