Without a valid VAT invoice, you shouldn’t claim the VAT. If you do, and HMRC query it, you’ll be liable to repay that amount to the taxman. You CANNOT reclaim VAT using a Pro-Forma invoice, order summary, statement or delivery note.

What happens if you incorrectly charge VAT?

If VAT is charged incorrectly on an invoice, then the invoice is not a valid VAT invoice and the customer cannot use the invoice to claim VAT. This applies even if the supplier has paid the VAT to HMRC. And it could be worse if HMRC believes that the error is deliberate or involves dishonesty.

Can you claim VAT back on sales?

The golden rule when claiming VAT back is you can claim only on goods and services that are used wholly and exclusively for your business. This means office supplies, computers and equipment, transport costs and services such as accountancy all count if they are solely used for the purpose of your business.

Can you be charged VAT retrospectively?

If your business isn’t registered for VAT, then you can’t charge VAT to your customers – but this also means that you can’t claim any VAT back. You have to register your business for VAT if its annual taxable sales are above the VAT registration limit.

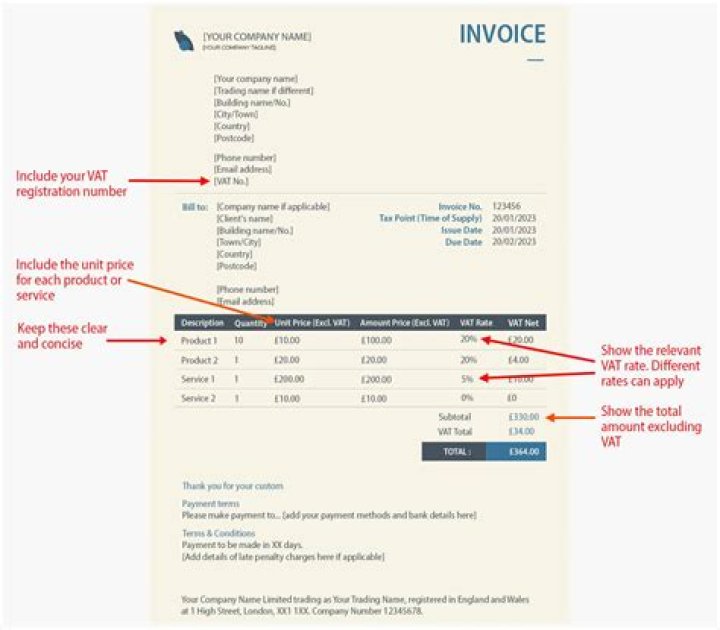

What is needed on VAT invoice?

£250 or less (including VAT), then you issue an invoice showing your name, address and VAT registration number the time of supply (tax point), a description which identifies the goods or services supplied, and for each VAT rate applicable, the total amount payable, including VAT shown in sterling and the VAT rate …

What is the difference between an invoice and a VAT invoice?

While a commercial invoice is simply the standard type of payment demand issued after the delivery of goods and services, VAT invoices have a much more specific purpose. In short, you must issue a valid VAT invoice to charge VAT on sales or reclaim VAT that you’re charged for goods and services.

When should you raise a VAT invoice?

Normally you must issue a VAT invoice within 30 days of the date you make the supply.

Is a VAT receipt the same as an invoice?

Both documents are fully itemised and contain a VAT breakdown and everything else you’d expect to find on a VAT invoice. The Sales Receipt doesn’t contain the word ‘Invoice’ on it and nobody’s ever queried that until today.

How many years can VAT go back?

If you’ve recently become VAT registered, you can reclaim VAT on some goods and services you bought before this point, but there is a time limit: On goods, you can reclaim VAT up to 4 years after you made the purchase. For services, you can reclaim VAT up to 6 months after the purchase.

If you don’t have a purchase invoice, you may still be able to recover the VAT provided you have sufficient alternative evidence and satisfy HMRC that the supply took place.

If you are registered for VAT, the general rule is that VAT can be reclaimed on goods and services bought by the business, known as input tax, as long as the business makes standard, reduced or zero-rates supplies. You will need to keep all invoices you receive as evidence to support your claim.

What is a valid VAT invoice?

A valid VAT receipt should include all of the following details: A unique invoice number. The tax date (the date of supply which is also known as tax point – if different from the invoice date) Your name or trading name and address (i.e. the customer) A description of the goods or services supplied to you.

What is needed for a valid VAT invoice?

A full VAT invoice needs to show: the supplier’s name, address and VAT registration number. the name and address of the person to whom the goods are supplied. a unique identification number (see below)

When was VAT incorrectly added to sales invoices?

The VAT inspector identified that the director was operating as a sole trader prior to incorporation and incorrectly adding VAT to the sales invoices. The business did not register for VAT until the date of incorporation 20th May 2008, but my client incorrectly raised VAT invoices to customers whilst a sole trader.

Can a customer claim VAT on an invoice?

If VAT is charged incorrectly on an invoice, then the invoice is not a valid VAT invoice and the customer cannot use the invoice to claim VAT. This applies even if the supplier has paid the VAT to HMRC. The customer, having claimed the VAT as input tax on their return, has submitted an “error” return.

Can a business charge the wrong amount of VAT?

Below are a couple of examples of common errors that businesses can make and how much VAT HMRC expects you to account for. A business makes a supply of goods another business subject to VAT at 20%. Due to a transposition error it charges the wrong amount of VAT. The sale is for £1150 plus VAT of £230, however, the invoice shows VAT of £320.

What happens if you claim too much VAT on your tax return?

The customer, having claimed the VAT as input tax on their return, has submitted an “error” return. If you have been charged too much VAT, the ONLY way to get it back is for the supplier to issue a credit note for the original amount and issue a new invoice showing the correct VAT rate/value.