In short the answer is no, you cannot offset rental losses against other income to reduce your tax bill.

How can I lower my tax on my rental income?

Here are 10 of my favourite landlord tax saving tips:

- Claim for all your expenses.

- Splitting your rent.

- Void period expenses.

- Every landlord has a ‘home office’.

- Finance costs.

- Carrying forward losses.

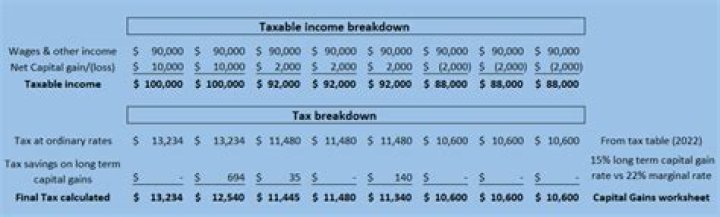

- Capital gains avoidance.

- Replacement Domestic Items Relief (RDIR) from April 2016.

Is insurance an allowable expense for rental income?

Yes! As a landlord, you can claim certain costs as a business expense when calculating the amount of Income Tax that you owe. This means that the cost of insuring your property is an allowable expense and is therefore tax deductible.

Can you use 100% of rental income as an offset?

Now, rental properties that are not the subject of the mortgage are close to 100% rental offset. 100% rental income less PITH (Principle, interest, property taxes, heat and condo fees) on the property. Rental properties that are subject of the mortgage can only use 50% of the rental income to qualify.

How to calculate gross debt service with rental offset?

Here is how rental offset comes into play when calculating the Gross Debt Service (GDS) ratio: GDS (with Rental Offset) = [PITH – (Rental Offset x Rental Income)] / Borrower’s Income Rental add-back is also defined as the percentage of rental income that a lender will allow a borrower use to help them qualify for a mortgage.

What’s the difference between a rental offset and a rental add-back?

Rental offset is the percentage of rental income that a lender will allow a borrower to deduct from their housing expenses to help them qualify for a mortgage. Typically the offset is in the range of 50-80% with a few lenders allowing up to 100% on conventional mortgages.

What’s the difference between GDS and rental offset?

GDS (with Rental Offset) = [PITH – (Rental Offset x Rental Income)] / Borrower’s Income Rental add-back is also defined as the percentage of rental income that a lender will allow a borrower use to help them qualify for a mortgage.