Backdating VAT Flat Rate Scheme Registration If you are registering for VAT and FRS at the same time, your VAT/FRS registration can often be backdated to the point when you request your VAT registration to commence. Surprisingly this can even be up to a year ago.

How do I get out of the flat rate scheme?

You can choose to leave the scheme at any time. You must leave if you’re no longer eligible to be in it. To leave, write to HMRC and they will confirm your leaving date. You must wait 12 months before you can rejoin the scheme.

What is monthly flat rate?

Monthly flat rate is the method to calculate the total interest expense for an instalment loan. Total interest amount = Principal Amount x Monthly flat rate x Tenor. Interest payable is calculated on the basis of “Rule of 78”. More interest will, in general, be included in earlier instalments, and less on principal.

Can you back date a VAT registration?

you may allow registration no further back than four years from the date the application is received, subject to the trader having an entitlement to registration for the whole of that period. you should not normally allow retrospective registration to an earlier date.

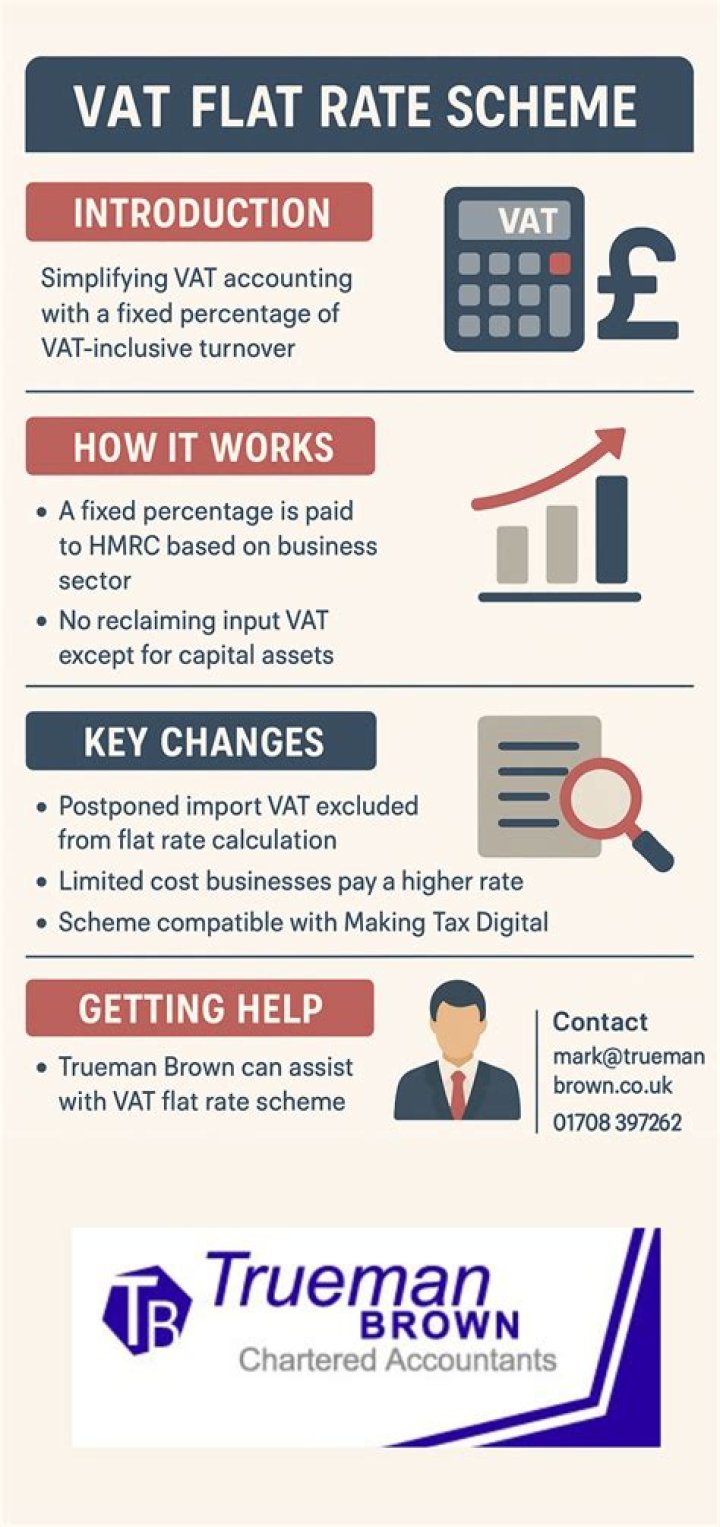

How do I claim VAT back on flat rate scheme?

You can’t reclaim VAT when you’re using the Flat Rate Scheme, unless you buy a capital asset that cost over £2,000 including VAT – you can reclaim the VAT on that, but must pay standard VAT on that asset when you sell it on. The VAT Flat Rate Scheme is designed to save a small business time, rather than cash.

What can you claim back on flat rate scheme?

Companies on the Flat Rate Scheme are unable to claim back any VAT on purchased goods and expenses for their business. However, you can reclaim VAT on capital asset purchases over £2,000, for example, a PC.

How is flat rate VAT calculated?

You calculate the tax you pay by multiplying your VAT flat rate by your ‘ VAT inclusive turnover’. Example You bill a customer for £1,000, adding VAT at 20% to make £1,200 in total. You’re a photographer, so the VAT flat rate for your business is 11%. Your flat rate payment will be 11% of £1,200, or £132.

How far back can I VAT register?

4 years

From your date of registration the time limit is: 4 years for goods you still have, or that were used to make other goods you still have. 6 months for services.

How does VAT flat rate scheme work?

Under the flat rate VAT scheme, you charge clients and customers the current standard VAT rate on all invoices (currently 20%), however you pay HMRC a flat rate of your turnover when returning VAT each quarter, and can’t reclaim for VAT paid on purchases as this is already factored in to the percentage.

Should I use VAT flat rate scheme?

Advantages: Using the flat rate scheme makes calculating the amount of VAT owed to HMRC extremely straightforward as well as minimising the amount of time spent on administrative tasks. Smaller businesses often lack the expertise or funds to keep records of VAT charges, and this scheme largely expedites this process.

Is it possible to backdate VAT and use the flat rate scheme?

Started to trade a few years ago didn’t register for vat. Is it possible to register now , back dating to date of incorporation and using the FRS from that date? He would just have to reissue his sales invoices from incorporation with the vat included . He would then stand to make a hefty flat rate profit. Is this ok? It seems wrong . Tags Quote

How do I apply for flat rate VAT?

Use form VAT600FRS to apply to join the Flat Rate VAT Scheme. If you’re using an older browser, for example, Internet Explorer 8, you’ll need to update it or use a different browser. Find out more about browsers. You’ll need to fill in the form fully before you can print it.

Is there any way to backdate VAT deregistration?

In other words, there is no scope to backdate the request – it will either be processed from the date when HMRC receives the request or a later date. Many businesses may want to deregister on 31 March 2017 (if they are eligible) to avoid being classed as a limited cost trader within the flat rate scheme.

When to set up DDI for flat rate VAT return?

For example, if your flat rate VAT return is due on Tuesday 7 September, 2 bank working days before this is Friday 3 September. If your return due date falls on a weekend or bank holiday you will need to set up your DDI at least 3 bank working days before the return is due.