Understanding income protection policies You are allowed to have multiple income protection policies, and there are legitimate reasons why people choose more than one product. You would typically be limited to a combined maximum of 75 per cent across the policies.

What is an income replacement benefit?

Income-replacement benefits are payments made to a person who, as the result of an automobile accident, becomes unable to work. In general, income-replacement benefits will be equal to 70% of your gross weekly income before the accident provided you were employed and not self employed.

At what age does income protection stop?

Most income protection policies will cover you until you turn 60, 65, or 70 years old, depending on your insurer and their guidelines. With most policies, you’ll also be covered by income protection insurance until one of the following happens: You cancel your policy. You’re unable to pay your premiums.

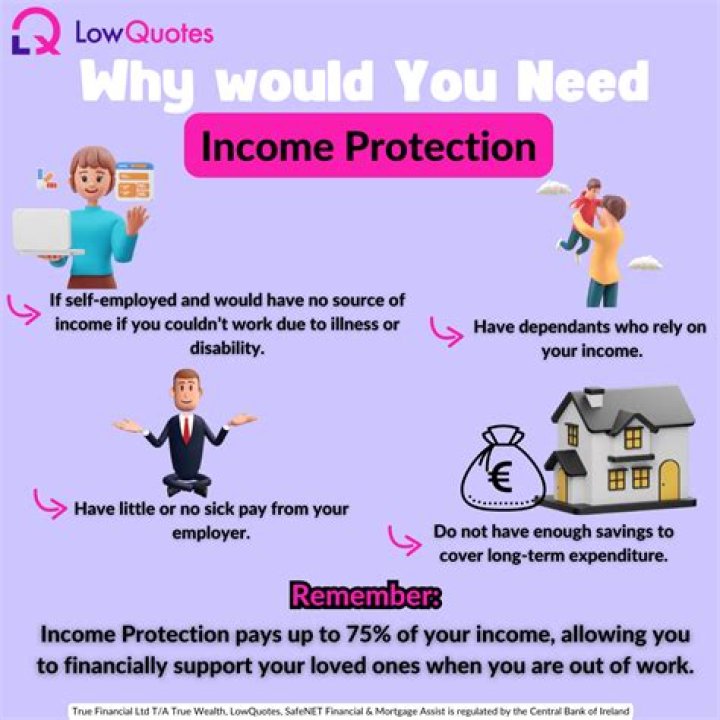

What happens if you have two income protection policies?

Income protection benefits are capped at 75% of your income. This means if you have two income protection policies and claim on both, your total payout from both will still equal 75% of what you earn. So by having more than two policies, you may be paying for benefits you won’t receive.

Is income replacement considered income?

Reporting wage and replacement benefits Revenue Canada requires you to report wage replacement benefits as income; however, this amount is not considered to be taxable income.

How many times can you claim income protection?

Each time you make a claim that’s accepted, you can be paid for up to 5 years, as long as you’re still unable to work due to the sickness or injury during that time. You can claim as many times as you need over the life of the policy.

You are allowed to have multiple income protection policies, and there are legitimate reasons why people choose more than one product. You would typically be limited to a combined maximum of 75 per cent across the policies.

What is the income replacement method?

The income replacement approach is a method of determining the amount of life insurance you should purchase. Under this approach, the insurance purchased is based on the value of the income the insured breadwinner can expect to earn during his or her lifetime.

Income replacement assistance generally means any gross weekly payments for loss of income that you are receiving or can receive because of the accident by law or under an income continuation benefit plan. For example, income replacement assistance includes short term disability and long term disability payments.

When can you claim income protection?

Time limits do apply to lodging income protection claims (usually six months from the time you become ill or injured), so you should lodge a claim as soon as possible after the illness or injury occurs and you are unable to return to work.

What happens if you have 2 income protection policies?

How do you calculate income replacement needs?

To get an estimate, take your annual income and multiply it by how many years you want to replace. People often choose five to ten times their annual income. Keep in mind, people with older dependents might not need income replacement as long as those with younger dependents.

What happens to an income replacement term insurance plan?

An income replacement term insurance plan is a death benefit plan. There is no maturity benefit. If the life assured passes away during the policy period, the nominee would receive a percentage of sum assured every month as an income replacement due to the loss of the income.

Where can I find an income replacement plan?

If you are unable to work due to injury or illness, Income Replacement plans provide a regular monthly payment. Compare and find the best plans at policybazaar.com. Income replacement plans are nothing but another name for TERM INSURANCE!

Can You claim income replacement on a slip and fall claim?

The person or entity responsible for paying your damages is usually entitled to deduct any other benefit amounts from the amount of your lost future or past income like: Income Replacement Benefits. For slip and fall claims, the at-fault party may receive credit for income received from other sources but only under certain circumstances.

How are income replacement benefits calculated in Ontario?

If you were employed at the time of the crash, your benefits generally will be calculated based on: your gross income in the four weeks preceding the crash, multiplied by 13. Your final benefit amount will be reduced in accordance with any other source of income replacement you receive.