Goods you cannot get a refund for You cannot get a VAT refund for: mail order goods, including internet sales, delivered outside of Northern Ireland. goods you’ve already used in Northern Ireland or the EU, such as perfume.

Is VAT input refundable?

A VAT vendor will be entitled to a VAT refund when the input tax paid on supplies to the vendor for a period exceeds the output tax charged by the vendor. During the period when the capital asset, which is likely to be utilised over many periods, is purchased, the input tax may exceed the output tax for the period.

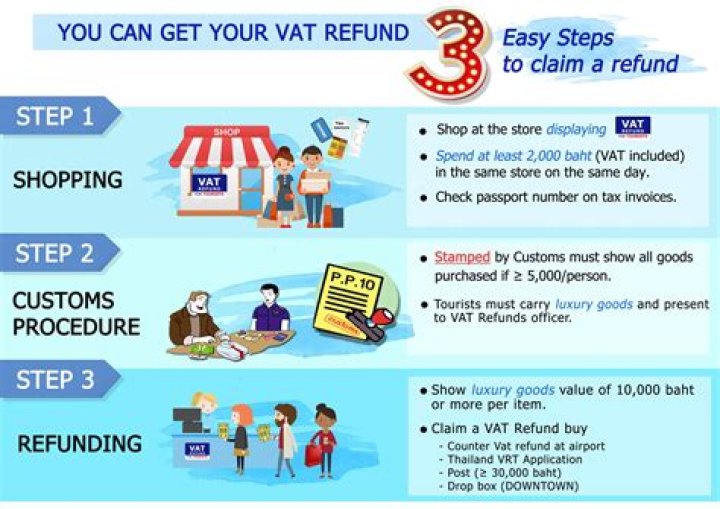

What purchases are eligible for VAT refund?

There are special rules for reclaiming VAT for:

- individual computers and single pieces of computer equipment costing £50,000 or more before VAT.

- aircraft, ships and boats costing £50,000 or more before VAT.

- land and buildings costing £250,000 or more before VAT.

How are VAT refunds paid?

Repayments are usually made within 30 days of HMRC getting your VAT Return. Your repayment will go direct to your bank account if HMRC has your bank details. Otherwise HMRC will send you a cheque (also known as a ‘payable order’). Contact HMRC if you have not heard anything after 30 days.

Can I claim VAT back on EU purchases?

If you reside in England, Scotland or Wales and visit Europe for less than 6 months, we have some good news for you – you can claim a VAT refund on your purchases!

Can you claim VAT back on alcohol gifts to staff?

There is no direct tax relief available if the gift is food, alcohol or tobacco.

What happens if I don’t claim back the VAT in the correct VAT period?

4.8 If you do not correct VAT errors and HMRC finds them If we find underdeclarations of VAT on your returns, we will assess for the tax due and may charge interest. You may also face a misdeclaration penalty.

Can you claim VAT without a receipt?

You can reclaim VAT on supplies of £25 or less without a receipt, with the caveat that you can show that the supplier is VAT registered.

How long do you have to reclaim VAT on purchases?

What’s the time limit for making a claim? You have up to 4 years to claim back any input VAT suffered for which you didn’t make a claim previously. However the 4 year time limit runs from the due date of the VAT return on which you should have made the original claim, rather than the date of the VAT invoice itself.