Now FHL losses can be carried forward and offset only against future profits from the same rental business. For this purpose a taxpayer’s UK FHLs are treated as one business and their EEA FHLs as another; losses from one cannot be offset against profits on the other.

Can furnished holiday lettings losses?

As with other let property, furnished holiday lettings in the UK form a separate business to furnished holiday lettings in the EEA. The losses cannot be relieved against the profits of a non-furnished holiday lettings property business nor against the profits of an EEA furnished holiday letting business.

How much tax will I pay on my holiday let?

Business Asset Disposal Relief (Entrepreneurs Relief) means that when it comes time to sell your furnished holiday let you should only be liable to pay under Entrepreneurs Relief only 10% on any capital gains during the time that you owned the property as a posed to the 18% currently levied on buy-to-let property …

What is a 12 month holiday restriction?

Twelve months’ holiday use doesn’t mean that you can use your holiday home for a whole year continuously or as your main residence. In short, it means that you can visit your home, or let it commercially, at any time of the year. Increasingly, holiday parks are opening up 12-month seasons.

Does furnished holiday let qualifying entrepreneurs relief?

A further CGT relief available to individual landlords of commercial furnished holiday lettings is entrepreneurs’ relief (ER). A CGT rate of 10% broadly applies to qualifying gains, up to a lifetime limit of £10 million. ER is not generally available on the disposal of a buy-to-let property rental business.

What does 12 month season mean?

Can you live permanently in a lodge?

Can you live in a holiday home on a park all year/permanently? No, you can’t live on a holiday park permanently. In short, a holiday home is not classed as a permanent residence; this also explains why you don’t pay council tax or stamp duty on holiday homes, static caravans and lodges!

How long can I carry forward property losses?

PIM4210 – Losses: setting losses against future profits The property business profit of the current year may be too small to give relief for all the loss of the previous year. In that case the unused part of the loss is carried forward to the next year; and so on indefinitely until relief can be given.

What can you do with FHL losses?

8. What you can do with losses. If your UK FHL business makes a loss, you can set the loss against your UK FHL profits of later years. Similarly, if your EEA FHL business makes a loss, you can set the loss against your EEA FHL profits of later years.

Can I carry back property losses?

Losses can only be carried forward and set off against future profits of the same property business.

Can a FHL loss be offset against EEA profit?

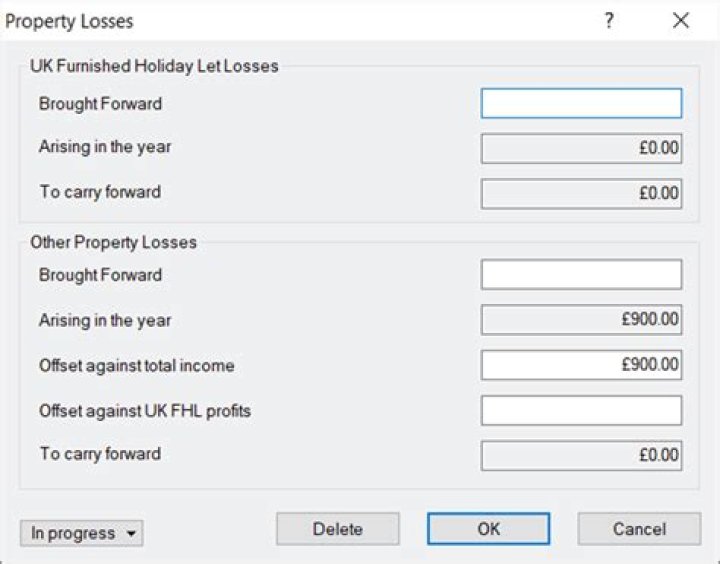

FHL losses can be carried forward and offset only against future profits from the same rental business. For this purpose, a taxpayer’s UK FHLs are treated as one business and their EEA FHLs as another; losses from one cannot be offset against profits on the other. Nor can the losses be set against other non-FHL rental income.

Can a non FHL property loss be set sideways?

Yes… but neither can non-FHL property losses generally be set sideways (for instance against FHL profits). Non-FHL losses can be set against FHL profits though, because they’re within the same (UK or overseas) property business. My point is that s 127 doesn’t get touched.

Can You offset holiday letting losses against other income?

You can no longer offset furnished holiday letting losses against other income. This change came into effect from the tax year ending 5 April 2012. You can only offset furnished holiday letting losses against future profits from the same property. For further information read ‘ What you can do with losses’ of the HMRC helpsheet.

Can a holiday letting business be a FHL?

From 2011/12 losses from a UK furnished holiday business can only be set against profits from the same UK furnished holiday letting business. You appear to be interpreting “losses from a UK FHL” as being “losses from a UK FHL after being set against other non-FHL property losses”.