Typically, the supply of goods with installation services is treated as a single transaction subject to VAT in the country where the goods are installed or assembled. This generally triggers an obligation to register for VAT under the EU VAT Directive.

What is VAT place of supply?

For VAT purposes, the place of supply of a service is the place where that service is treated as being supplied. This is the place where it’s liable to VAT (if any).

What is supply and install?

A Supply & Install Agreement is for businesses that offer both a product and an installation service for the product. Types of businesses that use Supply & Install Agreements include businesses that sell and install blinds and shutters, cabinet makers, air conditioning providers, fence suppliers and more.

Do you charge VAT on services supplied us?

The majority of goods exported to the US can be zero-rated for VAT. In other words, you do not need to charge VAT on the exported goods, or the extra charges such as shipping and delivery. Therefore, if you do several exports to the US, it may be beneficial to not be on the Flat Rate Scheme.

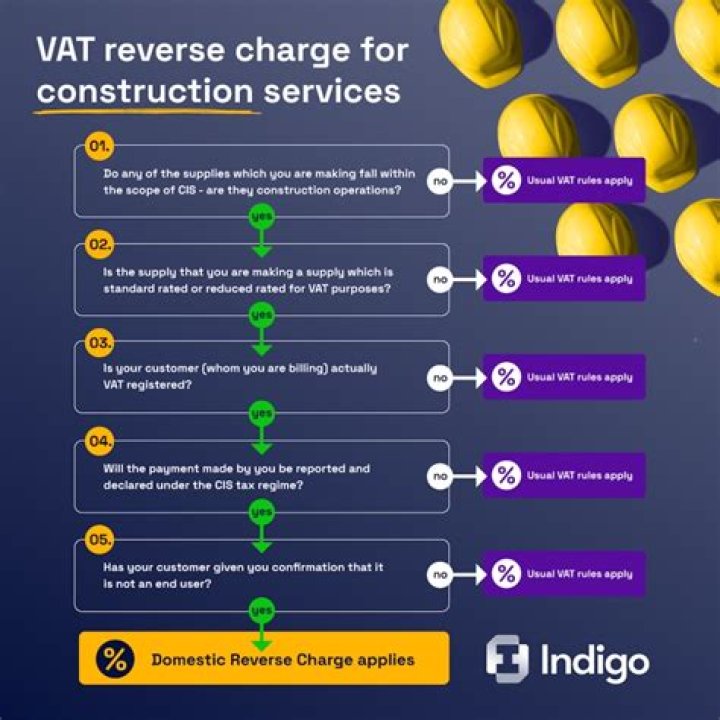

Do all builders charge VAT?

VAT for most work on houses and flats by builders and similar trades like plumbers, plasterers and carpenters is charged at the standard rate of 20% – but there are some exceptions. How you report and pay VAT in the construction industry is changing from 1 October 2019. Find out what you need to do to prepare.

What is place of supply rules?

Place of Supply – No Movement of Goods

| Supply Type | Place of Supply |

|---|---|

| No movement of goods, either by the supplier or by the recipient | Location of those goods at the time of delivery to the recipient (at the time of ownership transfer) |

| Goods are assembled or installed at site | Place of installation or assembly |

What is installation in business?

Installations are high priced capital or industrial products. They are costly, durable and are the main equipment of business users. In other word, the big, costly and long lasting machines necessary for business uses are called installations.

How do you find time of supply?

CGST/SGST or IGST must be paid at the time of supply. Goods and services have a separate basis to identify their time of supply. Let’s understand them in detail….A. Time of Supply of Goods

- Date of issue of invoice.

- Last date on which invoice should have been issued.

- Date of receipt of advance/ payment*.

How many types of supply are there?

Taking into account the two definitions of supply viz., composite supply and mixed supply, one can understand the essential statutory differences between the two kinds of supply.

What are the types of installation?

Types

- Attended installation. On Windows systems, this is the most common form of installation.

- Silent installation.

- Unattended installation.

- Headless installation.

- Scheduled or automated installation.

- Clean installation.

- Network installation.

- Bootstrapper.

A Supply & Install Agreement is for businesses that offer both a product and an installation service for the product. The Supply & Install Agreement is a contract between this business and its customers (whether they be residential or commercial customers).

What is the two third rule?

: a political principle requiring that two thirds rather than a simple majority of the members of a politically organized group must concur in order to exercise the power to make decisions binding upon the whole group — compare majority rule.

Do you pay VAT on supply of goods with installation?

VAT is due in the UK Supply of goods with installation is treated as a single transaction subject to VAT in the country where the goods are installed or assembled. UK VAT is therefore applicable on the transaction.

What does supply of a service mean in VAT?

For VAT purposes, a supply of a service is generally any commercial activity other than a supply of goods. The VAT rate should also be considered and will be dependent on the underlying good/service being supplied. Then look to whether you are supplying to a private consumer (B2C) or a business customer (B2B).

What are the rules for supply and installation?

VAT: Rules on supply and installation Typically, the supply of goods with installation services is treated as a single transaction subject to VAT in the country where the goods are installed or assembled. This generally triggers an obligation to register for VAT under the EU VAT Directive.

Is there VAT on goods shipped from Romania to the UK?

The materials will be shipped from the Romania to The United Kingdom and installed by your company. VAT is due in the UK Supply of goods with installation is treated as a single transaction subject to VAT in the country where the goods are installed or assembled. UK VAT is therefore applicable on the transaction.