If you complete a Self Assessment tax return, report any interest earned on savings there. You need to register for Self Assessment if your income from savings and investments is over £10,000.

Is it necessary to show savings account interest in ITR?

Interest earned from bank fixed deposits is fully taxable for individuals, while senior citizens can claim a deduction of up to ₹50,000 against the interest earned on savings and fixed deposit interest. Senior citizens claiming deduction, have to show it in the income tax return (ITR).

What is interest on self assessment tax?

HMRC will charge interest on any tax owing and on the penalties and charges incurred as a result of the late payment of tax owed. Currently they charge interest at a rate of 3%.

How can I check my savings account interest in ITR?

You can avail deduction of up to Rs 10,000 on the total savings account interest income earned. This deduction can be availed under Section 80TTA of the Income Tax Act and is available to an Individual and HUF. If your total interest income is below Rs 10,000 then you do not have to pay tax on it.

Is tax automatically deducted from bank interest?

Since 6 April 2016 your interest has been paid ‘gross’ Up to and including 5 April 2016 banks and building societies automatically deducted income tax from the interest you received on non-ISA savings and current accounts, unless you were registered for gross interest.

How much amount of interest is tax free?

For a residential individual (age of 60 years or less) or HUF, interest earned upto Rs 10,000 in a financial year is exempt from tax. The deduction is allowed on interest income earned from: savings account with a bank; savings account with a co-operative society carrying on the business of banking; or.

If you’re not employed, do not get a pension or do not complete Self Assessment, your bank or building society will tell HMRC how much interest you received at the end of the year. HMRC will tell you if you need to pay tax and how to pay it.

Is bank interest counted as income?

Most interest income is taxable as ordinary income on your federal tax return, and is therefore subject to ordinary income tax rates. Generally speaking, most interest is considered taxable at the time you receive it or can withdraw it. …

If you are doing a Self-assessment for 2015-16 then your bank interest will have been taxed at source and you declare the net-of-tax amount just as you did the previous year. HMRC gross it up and add it into their calculations but you won’t pay any extra tax on it unless your total income puts you into the 40% tax bracket.

Where does interest go on a self assessment tax return?

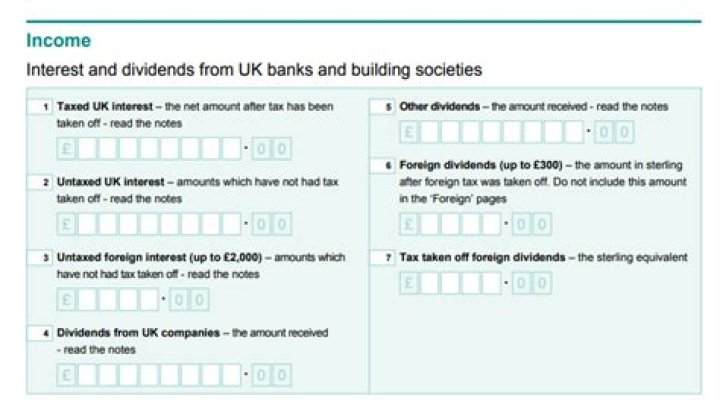

When declaring interest received on bank accounts, be sure to include: You can add taxed and untaxed interest to the ‘Main Return’ page of your Self Assessment tax return in your FreeAgent account.

When do you need to do self assessment on savings?

You need to register for Self Assessment if your income from savings and investments is over £10,000. Check if you need to send a tax return if you’re not sure. If you’re not employed, do not get a pension or do not complete Self Assessment, your bank or building society will tell HMRC how much interest you received at the end of the year.

What should I avoid on my self assessment tax return?

Here are some useful tips to help you avoid the most common mistakes people make in the rush to file before the Self Assessment deadline each year. The main section of your tax return must include the interest you received on all your bank accounts for the tax year in question.