Tax. Employees who’ve been made redundant only pay tax on payments over £30,000. They do not pay any National Insurance. Tax and National Insurance are deducted from other termination payments, for example payment in lieu of holiday or notice.

Is employer NI due on redundancy payments?

Termination payments will remain exempt from employee’s national insurance contributions.

Do you get taxed on redundancy pay UK?

Calculate your redundancy pay. Redundancy pay (including any severance pay) under £30,000 is not taxable. Your employer will deduct tax and National Insurance contributions from any wages or holiday pay they owe you.

Are redundancy payments classed as income?

Your redundancy payment won’t be treated as income when working out how much benefits you can get. It will be treated as capital. This means that the amount you get in redundancy payment will be added to any other savings you have.

What is the tax free amount for redundancy payments?

The tax-free limit is a flat dollar amount plus an amount for each year of service you complete in your period of employment with your employer. Indexation changes the tax-free limit on 1 July each year. Your employer will report the tax-free amount as a lump sum on your income statement or PAYG payment summary – individual non-business.

When do you have to pay redundant employees?

You must make the payment when you dismiss the employee, or soon after. A redundant employee also has the right to a written statement setting out the amount of redundancy payment and how you worked it out.

How are Redundancy Payments reported on the income statement?

Your employer will report the tax-free amount as a lump sum on your income statement or PAYG payment summary – individual non-business. Certain redundancy payments are tax-free up to a limit based on the number of years you worked for that employer.

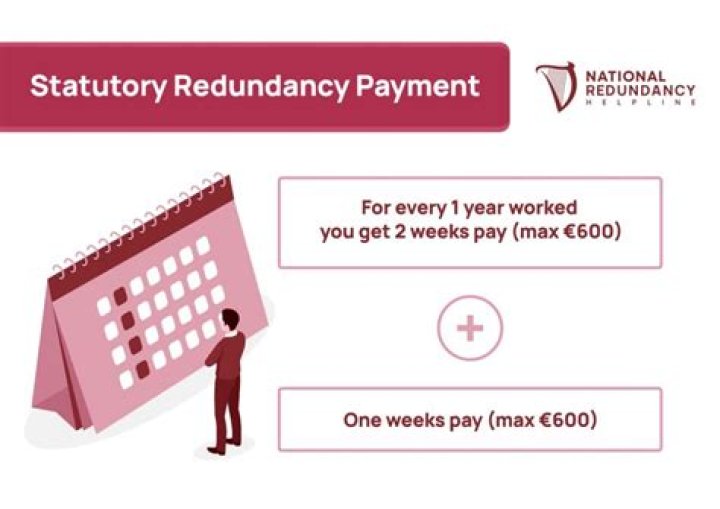

Is there a limit on a statutory redundancy lump sum?

The statutory redundancy lump sum, A payment made on account of death, injury or disability, (subject to a maximum lifetime tax-free limit of €200,000) Certain payments made by employers to employees arising from employment law rights claims.