Points to remember when filling in box 1:

- deduct any VAT on credit notes issued by you.

- deduct any VAT when you make refunds under the Retail Export Scheme.

- include VAT on the full value of the goods where you’ve taken something in part exchange.

- leave out any amounts notified to you as assessments by us.

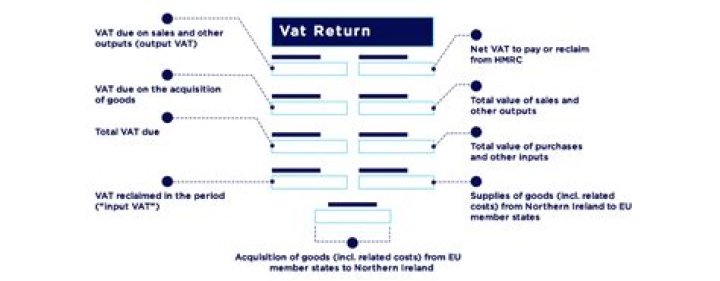

What is Box 3 on VAT return?

Box 3: total VAT due It is the amount of VAT due to HMRC. For returns completed online, this figure is worked out automatically by HMRC (see the Submitting online VAT returns guidance note).

How do companies do VAT returns?

Submit your VAT Return online

- Getting online. If you need:

- HMRC ‘s free online service. Sign in to your VAT online account and complete your VAT Return.

- Using accounting software. Most accounting software lets you submit your VAT Return to HMRC directly.

- Using accountants or agents.

- Help with online services.

What is Box 8 on VAT return?

Notes from HMRC: “In box 8 show the total value of all supplies of goods and related costs, excluding any VAT, to EU Member States from Northern Ireland.”

Is exempt VAT included in VAT return?

In a VAT registered business, sales and purchases of all goods and services except those deemed non-VATable, such as wages, loans, bank transfers, etc., must be included in the VAT Return. This means that even if they are zero-rated or exempt, so no VAT is actually due, their value must still be included in box 6 or 7.

When did reverse charge VAT come into effect?

1 March 2021

The VAT domestic reverse charge for construction came into force on 1 March 2021. It was initially planned to start from October 2019 but was postponed to October 2020 to “avoid the changes coinciding with Brexit” and “to help businesses and give them more time to prepare” according to HMRC.

Do wages go on a VAT return?

But do not include the value of any of the following: wages and salaries. PAYE and National Insurance contributions. money taken out of the business by you.

What is Box 2 on VAT return?

According to guidelines set out by HMRC, Box 2 on your VAT return should be used to show any VAT on goods purchased from VAT registered business in other EC member states (B2B). Box 2 relates to goods and not services covered by the VAT reverse charg.

How often are VAT returns?

every 3 months

Overview. You usually submit a VAT Return to HM Revenue and Customs ( HMRC ) every 3 months. This period of time is known as your ‘accounting period.

When do I need to complete the VAT return box?

You will only need to complete this box if your company has supplied goods to another EC Member state. If that is relevant to you then you must state the total value of the goods or services that has been supplied including any related costs (such as delivery charges) excluding VAT.

What should be included in a vat3 return?

The VAT3 return records the Value-Added Tax (VAT) payable or reclaimable by you in your taxable period. The return should be completed as follows: T1 – VAT on sales. This figure is the total VAT due on your: supplies of goods and services; intra-Community acquisitions of goods; received services as appropriate. T2 – VAT on purchases

Where does VAT payable appear on tax return?

VAT payable appears in Box 1 + Payable. VAT reclaimable appears in Box 4 – Reclaim; often the same figure. HM Revenue & Customs are able, where necessary, to challenge and disallow any amount wrongly claimed in Box 4. If playback doesn’t begin shortly, try restarting your device.

What happens to my VAT return after Brexit?

After 01/01/2021 only applicable to acquisition of goods into Northern Ireland from EU. Including applicable VAT payable on imports under postponed VAT accounting shown in Box 1. Total value of sales and all other outputs excluding any VAT. Include your box 8 figure