You can usually get a copy of the P11D from your employer. If they cannot give you one, you can contact HMRC for a copy.

Do employers still issue P11D?

Unless your employer has agreed otherwise with HMRC, the P11D should also include any payments you have received from your employer as reimbursement of business expenses you may have paid personally. You employer is required to give you a copy of your P11D by 6 July following the end of the tax year.

When should P11D be completed?

6th July

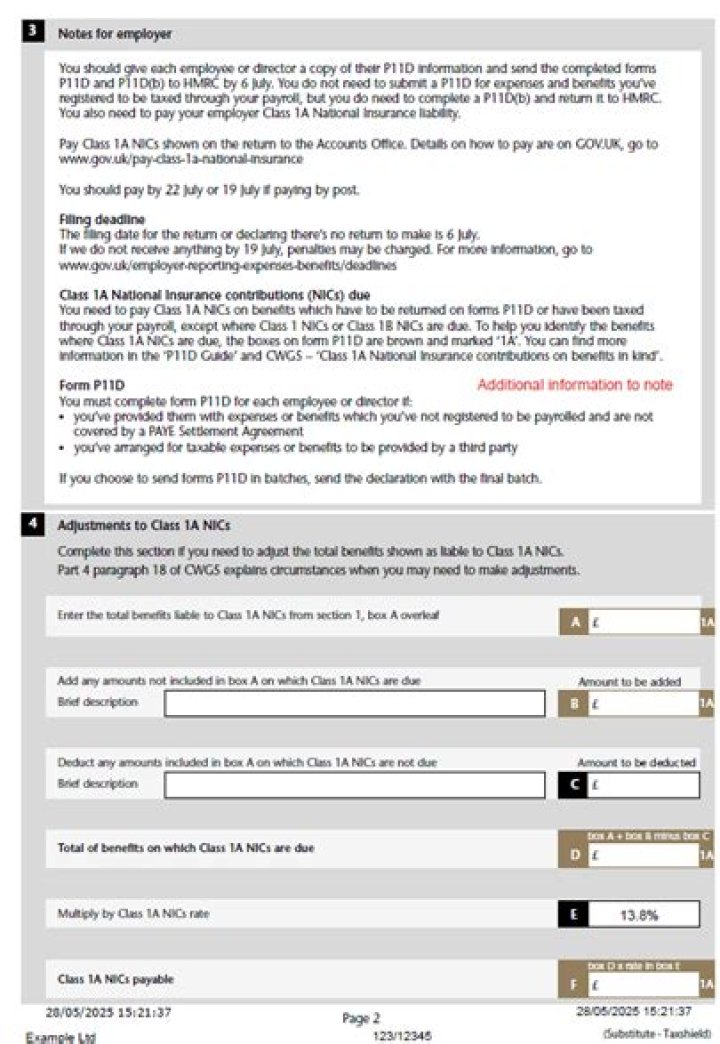

The P11D form must be filed with HMRC every year on the 6th July. Any tax due must be paid to HMRC by the 22nd July each year.

What do I do with a P11D?

Your employer will submit the P11d form each tax year to the tax office directly, and should give you a copy for your records. The P11D gives the tax office the details they need to update your PAYE record with the type and value of any company benefits you received during the tax year.

How is a P11D calculated?

To calculate annual company car tax the P11D value is multiplied by the percentage rate of income tax you pay (20% or 40%) and by the benefit-in-kind tax band dictated by the car’s carbon dioxide emissions. A list of current BIK tax bands can be found here, while our company car tax calculator can be found here.

Do I need to send P11D to employees?

You do not need to submit a P11D form for an employee if you’re paying tax on all their benefits through your payroll. You’ll still need to submit a P11D(b) form so you can pay any Class 1A National Insurance you owe.

Do ex employees get a P11D?

Regulation 94 (4) says that an employee who is not a current employee is not entitled to be sent a P11D or be sent one to their last known address. A ‘former employee’ is required to give the employer ‘notice’, i.e., they have to request one.

What happens if employer doesn’t provide P11D?

What if I don’t receive a P11D? You might not be given a P11D from your employer – it’s not a form they have to provide. If they don’t issue a P11D, they must tell you how much each benefit you’ve received is worth. You won’t be given a P11D if your employer takes the tax you owe on your benefits out of your pay.

When do employers need to send out P11D forms?

Employers are required to submit the P11D and P11D (B) forms on the 6th of July following the end of the tax year as well as giving individual copies for each employee. Employees should be given a copy of their form if they require it for their Self-Assessment Tax Return.

Why are benefits in kind not reported on P11D?

Benefits in Kind are the non-monetary value that employers provide to their employees on top of their normal salary. Some expenses and benefits in kind are exempt and therefore are not required to be reported in P11D. This exemption is typical when the employer pays the actual cost incurred in expense claims.

What happens if you are late paying your P11D ( B )?

You’ll get a penalty of £100 per 50 employees for each month or part month your P11D(b) is late. You’ll also be charged penalties and interest if you’re late paying HMRC.

When do I need to submit a P11D ( B ) to HMRC?

If HMRC have asked you to submit a P11D (b), you can tell them you do not owe Class 1A National Insurance by completing a declaration. You can deduct and pay tax on most employee expenses through your payroll (sometimes called ‘payrolling’) as long as you’ve registered with HMRC before the start of the tax year (6 April).