Accounting for business goodwill in your books requires that you subtract the fair market value of tangible assets from the total worth of the business. Goodwill is, therefore, equal to the cost of acquisition minus the value of net assets.

What is goodwill when purchasing a company?

Goodwill is an intangible asset that is associated with the purchase of one company by another. Specifically, goodwill is the portion of the purchase price that is higher than the sum of the net fair value of all of the assets purchased in the acquisition and the liabilities assumed in the process.

Is goodwill a liability to the purchasing company?

The goodwill amounts to the excess of the “purchase consideration” (the money paid to purchase the asset or business) over the net value of the assets minus liabilities. It is classified as an intangible asset on the balance sheet, since it can neither be seen nor touched.

What business type is goodwill?

intangible business asset

Goodwill is a type of intangible business asset. It is defined as the difference between the fair market value of a company’s assets (less its liabilities) and the market price or asking price for the overall company.

Does book value include goodwill?

Traditionally, a company’s book value is its total assets minus intangible assets and liabilities. However, in practice, depending on the source of the calculation, book value may variably include goodwill, intangible assets, or both.

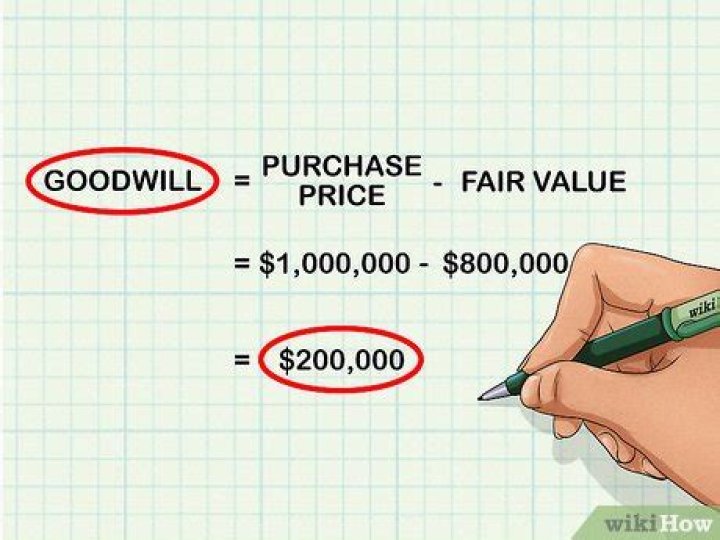

Subtract the book value from the purchase price to calculate Goodwill. Goodwill is defined as the price paid in excess of the firm’s fair value. To calculate it, simply subtract the total asset market value amount from the purchase price; this amount is nearly always a positive number.

Does goodwill impairment affect income statement?

The amount can change, however, if the goodwill declines. If that’s the case, the company undergoes what’s known as goodwill impairment. That’s because they must now record that $50,000 impairment as an expense on the income statement.

As a result, book value can also be thought of as the net asset value (NAV) of a company, calculated as its total assets minus intangible assets (patents, goodwill) and liabilities. Book value may also be known as “net book value” and, in the U.K., “net asset value of a firm.”

Why do companies pay for goodwill?

Goodwill is the premium that is paid when a business is acquired. If a business is acquired for more than its book value, the acquiring business is paying for intangible items such as intellectual property, brand recognition, skilled labor, and customer loyalty.

Where does the goodwill in a subsidiary come from?

For example, Company acquires business from sole trader, then later the company is bought by parent Have you considered the possiblity that the goodwill in the subsidiary comes from a different acquisition? For example, Company acquires business from sole trader, then later the company is bought by parent

What happens to the goodwill on an acquisition?

In the single entity the cost of acquisition will be shown as investment. Upon consolidation, this investment will be removed and replaced with the assets and liabilities of the subsidiary, with the difference being recognised as goodwill.

How are intangible assets and goodwill used to calculate goodwill?

The amount of goodwill is the cost to purchase the business minus the fair market value of the tangible assets, the intangible assets that can be identified, and the liabilities obtained in the purchase. To calculate goodwill, we should take the purchase price of a company and subtract the fair market value of identifiable assets and liabilities.

How is the excess purchase price of goodwill calculated?

Next, calculate the Excess Purchase Price by taking the difference between the actual purchase price paid to acquire the target company and the Net Book Value of the company’s assets (assets minus liabilities). 5. Calculate Goodwill