Work out your residence status You’re automatically resident if either: you spent 183 or more days in the UK in the tax year. your only home was in the UK – you must have owned, rented or lived in it for at least 91 days in total – and you spent at least 30 days there in the tax year.

183

Work out your residence status You’re automatically resident if either: you spent 183 or more days in the UK in the tax year. your only home was in the UK – you must have owned, rented or lived in it for at least 91 days in total – and you spent at least 30 days there in the tax year.

What counts as a day in the UK for tax purposes?

Days you are still physically in the UK at the end of that day, at midnight, count as days spent in the UK for the purposes of tax and residency. Been present in the UK on more than 30 days without being present at the end of that day in the tax year. These are called qualifying days.

What are the key dates for tax year 2011 / 12?

Key dates for the tax year 2011/12 England Reviewed 01/08/11 Directors’ Briefing Finance This briefing is a month-by-month schedule of important deadlines in the tax year 6 April 2011 to 5 April 2012. It will help you to prepare and send off the main forms in good time — to HM Revenue & Customs (HMRC) and Companies House.

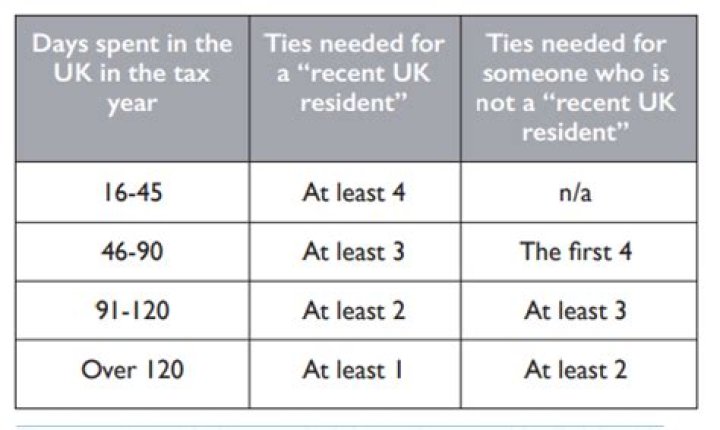

How long do you have to be resident in UK to pay tax?

Again, they are set out in detail in HMRC’s guidance, which you can find on GOV.UK. Broadly they are as follows: You have a home in the UK for a period of more than 90 days and you are present in the home on at least 30 separate days (note there are further conditions in relation to this test which you should also consider);

How many days do you have to live in UK to be considered UK resident?

You’re automatically resident if either: you spent 183 or more days in the UK in the tax year. your only home was in the UK – you must have owned, rented or lived in it for at least 91 days in total – and you spent at least 30 days there in the tax year.

When did the remittance basis for hmrc6 change?

ofHMRC6 for any tax liability that arises before 5 April 2011. Thisversion of the HMRC6 was last amended in October 2011 and does not reflect legislativechanges to the remittance basis introduced for tax year 2012–13 nor the introductionof the Statutory residence test in 2013–14.