Most financial planning studies suggest that the ideal contribution percentage to save for retirement is between 15% and 20% of gross income. These contributions could be made into a 401(k) plan, 401(k) match received from an employer, IRA, Roth IRA, and/or taxable accounts.

Is it better to contribute pre tax or after tax?

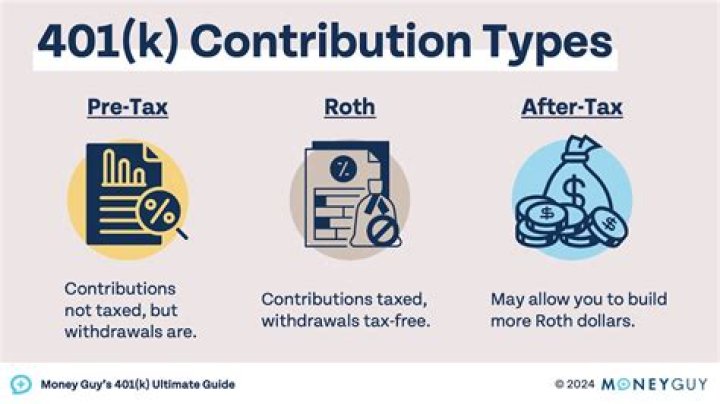

Pre-tax contributions may help reduce income taxes in your pre-retirement years while after-tax contributions may help reduce your income tax burden during retirement. You may also save for retirement outside of a retirement plan, such as in an investment account.

What is a pre tax bonus contribution?

The Elusive Pre-Tax Bonus Companies may use discretionary contributions as a performance-based, pre-tax bonus. Such discretionary company contributions are tax-deductible to the company, not currently taxable to the recipient employee and are not subject to payroll taxes, either from the company or the employee.

What are examples of pre tax contributions?

Pre-tax deductions: Medical and dental benefits, 401(k) retirement plans (for federal and most state income taxes) and group-term life insurance. Mandatory deductions: Federal and state income tax, FICA taxes, and wage garnishments. Post-tax deductions: Garnishments, Roth IRA retirement plans and charitable donations.

Is it better to pre-tax 401K or Roth?

The biggest benefit of the Roth 401(k) is this: Because you already paid taxes on your contributions, the withdrawals you make in retirement are tax-free. By contrast, if you have a traditional 401(k), you’ll have to pay taxes on the amount you withdraw based on your current tax rate at retirement.

Is Roth IRA pre or post tax?

Roth IRAs do not benefit from the same upfront tax break that traditional IRAs receive. The contributions are made with after-tax dollars. So, a Roth IRA will not reduce your tax bill for the year that you make contributions.