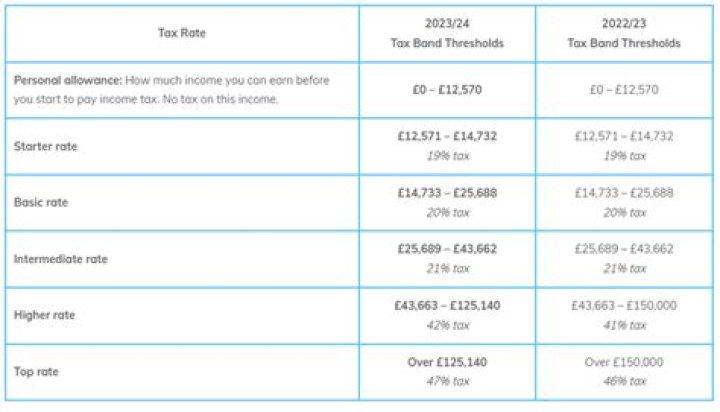

If your income is: Less than the basic rate threshold of £12,570 – you’ll pay 0% in tax on rental income. Above £12,570 and below the higher rate threshold of £50,270 – you’ll pay 20% in tax on rental income. Above £50,270 and below the additional rate threshold of £150,000 – you’ll pay 40% in tax on rental income.

How much rental income is tax free in UK?

Property you personally own The first £1,000 of your income from property rental is tax-free. This is your ‘property allowance’. Contact HMRC if your income from property rental is between £1,000 and £2,500 a year.

How does the Non-Resident landlord Scheme Work?

The NRLS is a scheme to tax the UK rental income of persons who have a usual place of abode outside the UK – known as non-resident landlords. It does this by imposing on the UK letting agent an obligation to withhold tax on the rental income before it is paid to the overseas landlord.

Can a non resident rent out a property in the UK?

Individuals that are non-residents of the UK and/or who have their “normal place of abode” outside the UK need to register with HMRC as non-resident landlords if they receive income from letting out UK property. If they do not, either the letting agent they appoint or the tenants must withhold 20% tax at source from the rental income.

How to get rental income paid in UK without tax?

To get your UK rental income paid without deduction of UK tax if you’re an individual landlord of a UK property and normally live outside the UK, you can: use the online service fill in form on-screen, print and post to HMRC

Do you have to file a UK tax return if you are a non resident?

If you are a Non-Resident Landlord and receive rental income in the UK, you will need to complete a self-assessment tax return each year to declare your income – even if no tax is actually payable here.

Do you have to register with HMRC if you are non resident?

HMRC continues to intensify its effort to collect tax owed by non-residents and from UK property income. Individuals that are non-residents of the UK and/or who have their “normal place of abode” outside the UK need to register with HMRC as non-resident landlords if they receive income from letting out UK property.