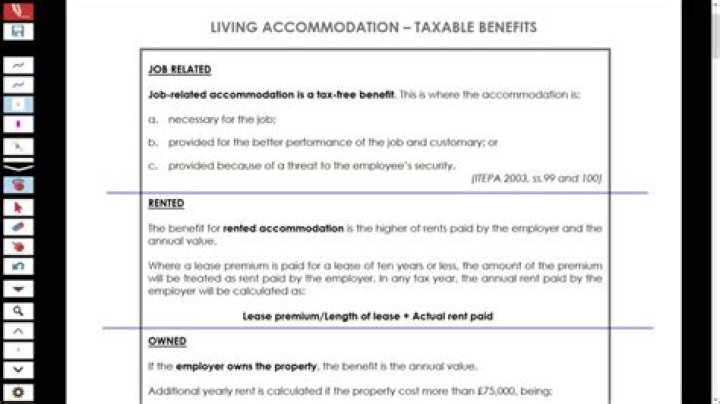

The Provision of Accommodation: Tax Liability The provision of living accommodation for an employee and/or members of the employee’s family or household gives rise to a taxable benefit unless the accommodation in question is exempt.

How is the value of living accommodation benefit in kind calculated?

The value of the accommodation benefit is calculated as follows:

- Defined value of the living accommodation; or.

- 30% of the gross income from employment (including wages, allowances, perquisites but not benefits-in-kind and share options perquisite)

- Whichever is lower.

What is the value of rent free accommodation?

Rent Free Accommodation – Leased by Employer In case of rent-free accommodation provided to an employee, wherein the employer has taken the property on lease or rent, the value of the perquisite would be the actual amount of lease or rental paid or 15% of the salary, whichever is lower.

What are living accommodations?

living accommodation means a building, recognised mobile home, or boat used as a dwelling, or occupied or available for occupation for residential purposes and includes any occupied yard, garden, outhouses, and appurtenances belonging to the building.

Can a company provide living accommodation for an employee?

Where living accommodation is provided for an employee or for members of their family or household by the employer it’s deemed to have been provided by reason of that employment. There are 2 exceptions to this.

Can a P9D company provide an employee with living accommodation?

No Class 1As apply where the living accommodation is provided to a P9D employee. In certain limited circumstances it is possible to provide an employee with tax-free living accommodation. This applies where:

Who is liable for tax on company provided living accommodation?

Subject to paragraphs 21.2 and 21.3 below, where an employee is provided with living accommodation by their employer (or by another person where the provision is by reason of the employment) the employee is liable to tax on the value of the accommodation provided.

Is the tax system fair for employer provided living accommodation?

The government believes that the tax system should be fair, easy to understand (for both employers and employees) and simple to administer, but recognises that the complexity within the current rules means that this may not be the case for employer provided accommodation.