VATSC06150 – Consideration: Payments that are not consideration: Capital contributions. If there is no evidence of the recipient being obliged to provide a benefit in return for the payment then it should be treated as outside the scope of VAT.

What is a capital contribution in a lease?

A capital contribution is a payment by a landlord to a tenant in respect of works to premises. They’re generally made on the grant of the lease, but can be made when works are required to the premises or on assignment of the lease.

Can a landlord claim capital allowances?

Claiming Capital Allowances on Equipment A landlord running a property rental business can claim capital allowances on equipment used for running the business, such as computers, office furniture and maintenance tools.

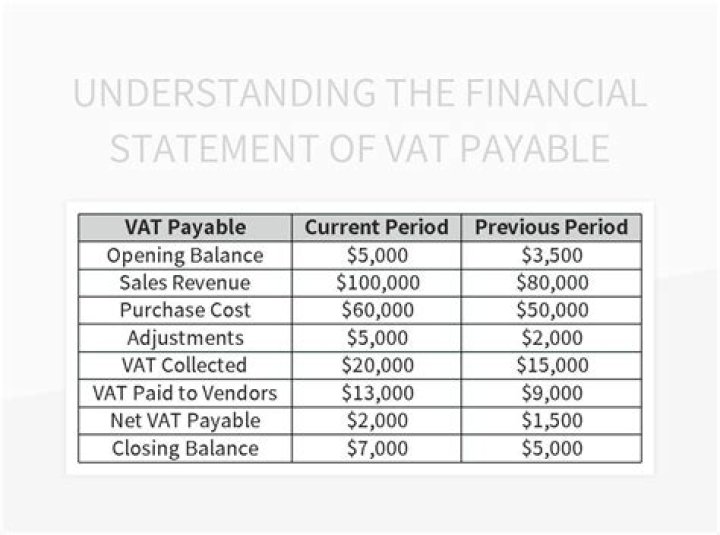

Do landlords have to pay VAT?

If the landlord has ‘opted to tax’ for VAT purposes, then the rental payments will be subject to VAT; otherwise, rental payments are exempt from VAT. If your business is VAT-registered, your costs will not normally be any higher whether the landlord has opted to tax or not.

What is a fit out contribution?

A Fitout Contribution is a payment from the Landlord (either as a lump sum or instalments over time) which is applied to the Tenant’s fitout works. Alternatively, the parties may pre-agree on the value of the Landlord’s contribution to the Tenant’s fitout and the Landlord carries out the works, up to that value.

Can landlords claim VAT back?

Buy-to-let landlords cannot usually reclaim VAT on their expenses. Whilst HMRC considers that renting out homes is a business for VAT purposes, it is an exempt one. This can be bad news for landlords because exempt businesses are prevented from reclaiming VAT paid on expenses.

Do you pay VAT on a reverse premium?

The payment of a reverse premium by the assignor to the assignee will have VAT on it.

Is VAT payable on a surrender premium?

If the Tenant has not exercised the option to tax, the surrender will be treated as exempt and no VAT will be payable by the Landlord on any premium paid by it. If the Tenant pays the Landlord to accept a surrender VAT will be payable if the Landlord has exercised the option to tax.