pre-approval

A pre-approval is a preliminary evaluation of a potential borrower by a lender to determine whether they can be given a pre-qualification offer. Pre-approvals are generated through relationships with credit bureaus which facilitate pre-approval analysis through soft inquiries.

investopedia.com › terms › preapproval

What are the stages of a mortgage application UK?

- Step 1: Contact a specialist broker. ...

- Step 2: Obtaining a 'Decision In Principle' ...

- Step 3: Your official mortgage application. ...

- Step 4: Valuing the property. ...

- Step 5: Getting your official mortgage offer.

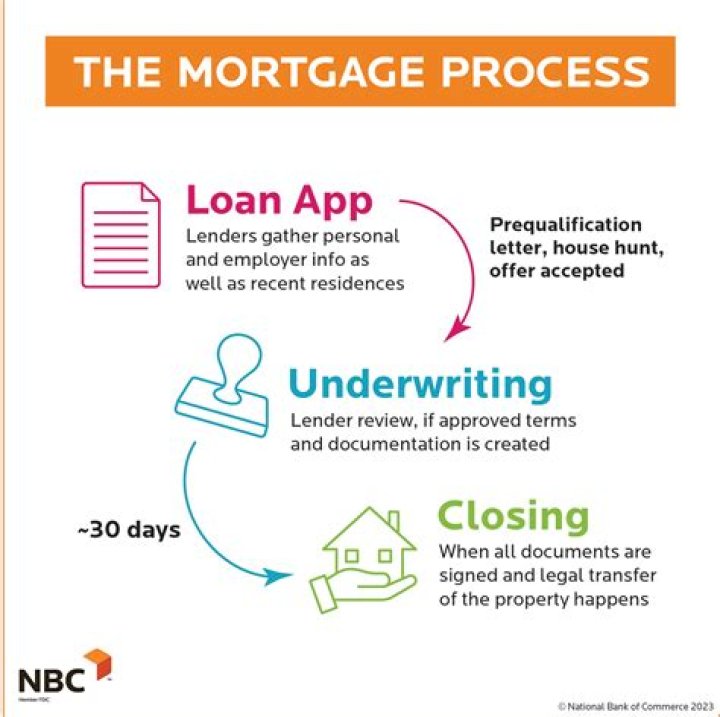

What is the timeline for mortgage loan process?

Understand the mortgage you can afford: two weeks. Find a home and make an offer: three to eight weeks. Secure a mortgage lender, home inspection and appraisal: five to six weeks. Complete mortgage underwriting and closing: two to four weeks.How do I know if my mortgage will be approved?

You'll have the best chances at mortgage approval if:

- Your credit score is above 620.

- You have a down payment of 3-5% or more.

- Your existing debts are low.

- You've had a stable job and income for at least two years.

What are the 6 elements of a mortgage application?

The six items are the consumer's name, income and social security number (to obtain a credit report), the property's address, an estimate of property's value and the loan amount sought.Mortgage Application Process UK | First Time Buyer Secrets

What is the 3 7 3 rule in mortgage?

Timing Requirements – The “3/7/3 Rule”The initial Truth in Lending Statement must be delivered to the consumer within 3 business days of the receipt of the loan application by the lender. The TILA statement is presumed to be delivered to the consumer 3 business days after it is mailed.

What happens after underwriting approval?

If your loan is approved, it means the underwriter has deemed you (and your co-borrower, if you have one) a trustworthy candidate and appropriate fit for the loan program you've applied for. At this point, you'll move forward to the next step of getting all your documents previewed and signed, then closing your loan.Is no news good news when waiting for mortgage approval?

When it comes to mortgage lending, no news isn't necessarily good news. Particularly in today's economic climate, many lenders are struggling to meet closing deadlines, but don't readily offer up that information. When they finally do, it's often late in the process, which can put borrowers in real jeopardy.Who actually approves a mortgage?

Step 2: Be patient with the review process. Once you've submitted your application, a loan processor will gather and organize the necessary documents for the underwriter. A mortgage underwriter is the person that approves or denies your loan application.How long does final approval take?

In general, it should take about 30 days from accepted offer through the date your loan closes. As a reminder, this is just a general timeline; the process can be faster or slower. There may be circumstances that change your timeline.Is underwriting the last step?

No, underwriting is not the final step in the mortgage process. You still have to attend closing to sign a bunch of paperwork, and then the loan has to be funded. The underwriting process itself can be smooth or “bumpy,” depending on your financial situation.How long does underwriting take for final approval?

Mortgage lenders have different 'turn times' — the time it takes from your loan being submitted for underwriting review to the final decision. The full mortgage loan process often takes between 30 and 45 days from underwriting to closing.How long does it take underwriter to clear to close?

Final Underwriting And Clear To Close: At Least 3 DaysOnce the underwriter has determined that your loan is fit for approval, you'll be cleared to close. At this point, you'll receive a Closing Disclosure.

What comes first underwriting or valuation?

Once the mortgage lender's underwriter has received a copy of your completed survey, they will be checking to see if the valuation makes sense and that there are no issues with the property highlighted in the report. From start to finish, the entire valuation process takes around 2 weeks to complete on average.Does valuation mean mortgage is approved?

Does Valuation mean Mortgage is Approved? A mortgage valuation does not mean that a mortgage is approved. Getting a mortgage valuation does not automatically mean that a mortgage is approved. This is because there are other requirements that the borrower needs to comply with.What happens after a mortgage application is submitted?

After submittingNow it's up to the lender. They'll review your application and documentation, and request a check on the property known as a lender's valuation. Based on their review of your application and the result of the valuation, they'll make their final decision on whether to lend, or not.

What are red flags for underwriters?

Red flags for underwriters are issues that arise during processing and are questionable. Different types of underwriters have their red flags to look out for, but in general, underwriters are tasked to find suspicious discrepancies in applications to better assess financial risks.What should you not do during underwriting?

Tip #1: Don't Apply For Any New Credit Lines During Underwriting. Any major financial changes and spending can cause problems during the underwriting process. New lines of credit or loans could interrupt this process. Also, avoid making any purchases that could decrease your assets.Why would I be denied after pre approval?

Changes In Your Credit ScoreIf your credit score has dropped below the minimum credit score requirements since you got pre-approved, your home loan application may still be denied. Your score may have dropped recently for a number of reasons, such as taking on new debt, making late, or missing payments.