VAT or Value Added Tax is a type of tax that is charged by the Central Government on the sale of services and goods to the consumers. VAT is paid by the producers of services and goods, but it is finally imposed on the consumers who purchase the services and goods when they pay for it.

What is VAT Value Added Tax briefly explain with the help of an example?

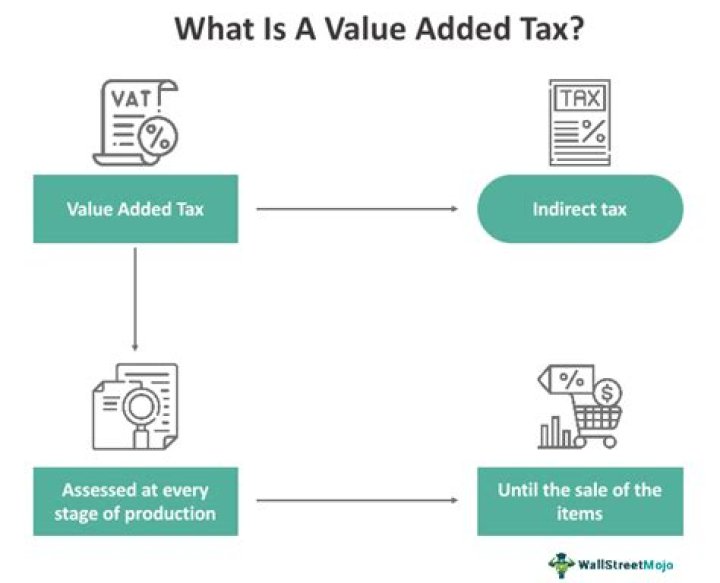

A value-added tax (VAT) is a consumption tax that is levied on a product repeatedly at every point of sale at which value has been added. For example, if a product costs $100 and there is a 15% VAT, the consumer pays $115 to the merchant. The merchant keeps $100 and remits $15 to the government.

Are there different types of VAT?

There are three rates of VAT which are applied to goods and services in the UK. Standard Rate (currently 20%), Reduced Rate (currently 5%) and Zero Rate (0%). VAT exempt items are outside of all VAT schemes and are not taxable.

What is my Value Added Tax?

the GST is levied at a rate of 5% (a reduced rate of 0% is also available for certain goods); the HST is levied at rates between 13% and 15% (with a reduced rate of 0%); the QST is imposed at a rate of 9.975%; the PST is levied at rates ranging between 6% and 8%;

Is VAT a direct or indirect tax?

There are also ‘indirect’ taxes, which are levied on goods and services. The most well-known example of an indirect tax is value added tax (VAT). This is less obvious than a direct tax as it is included in the price of things that you buy.

What is the difference between Value Added Tax and VAT?

What is a ‘Value-Added Tax – VAT’. A value-added tax (VAT) is a consumption tax placed on a product whenever value is added at each stage of the supply chain, from production to the point of sale.

What is the VAT Act?

Value Added Tax (VAT) is introduced by the Act No.14 of 2002 and is in force from 1st August, 2002. VAT Act replaced the Goods and Services Tax (GST) which was almost similar tax on the consumption of goods and services. It is a tax on domestic consumption of goods and services.

When was Value Added Tax introduced in the UK?

simplified value added tax (svat) scheme Value Added Tax (VAT) is introduced by the Act No.14 of 2002 and is in force from 1st August, 2002. VAT Act replaced the Goods and Services Tax (GST) which was almost similar tax on the consumption of goods and services. It is a tax on domestic consumption of goods and services.

What are the benefits of a VAT system?

Possible benefits of introducing a nationwide VAT tax include: Unlike our current income tax system, VAT doesn’t require taxpayers to file yearly tax returns and offers fewer opportunities for deduction loopholes, misreporting, and tax evasion. A VAT could serve as an efficient alternative to the United States’ current income tax system.