NT means no tax to pay on this income. Your employer is being instructed by HMRC not to deduct any tax from this income source.

What does tax code NT M1 mean?

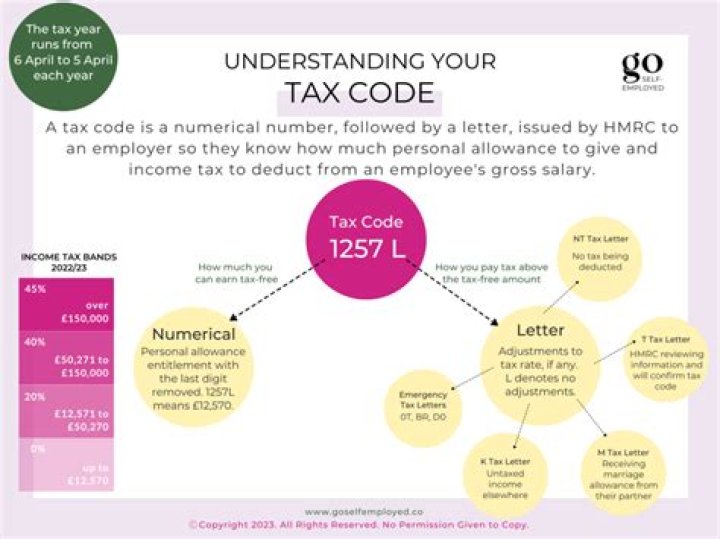

The NT code: when you pay no tax. W1 and M1: emergency tax codes.

What is a NT tax code?

Applying an NT code means that the employer does not have to operate PAYE on employment income relating to non-UK work duties, however this doesn’t relate to National Insurance contributions and this will have to be reviewed separately. …

How do I get my NT tax code UK?

How do I apply for an NT code?

- Telephone number: 0300 200 3300.

- Telephone number (Overseas): 00 44 135 535 9022.

What is tax code NT M1?

W1 and M1: emergency tax codes This normally ensures you receive the basic amount of monthly tax-free pay. But it doesn’t take into account any other relief or allowances. However, there will also be either W1 (for weekly pay) or M1 (for monthly pay).

Why would you have an NT tax code?

You have been given code NT because you are declaring income in another way that has been agreed by HMRC, perhaps because you have self employed income.

What does it mean to have NT code in UK?

An NT code means you won’t pay tax on the same income in the UK and your country of residence. Currently, if you do not have an NT code you would be on emergency tax in the UK.

When do I receive my NT tax code?

You will then receive your NT (Nil Tax) code. As a result, from here on in the gross amount will be withdrawn from your pension. But remember, it is your responsibility to declare this income in the country that you are resident.

Can a UK employer impose foreign tax on an overseas employee?

Where a UK employer has employees working abroad, an overseas Revenue authority may impose responsibilities for foreign tax in relation to the employees’ salaries on the overseas client of the UK employer. If so, send full details to IPD Technical (Earnings) with the employer’s accounts file.

Can a UK employee work in another country and still pay UK NICs?

Workers temporarily posted by their UK employer to one of these countries may be able to continue paying contributions to the UK instead of to the country you post them to. If this is the case, apply to HMRC for a ‘Certificate of Continuing Liability’ for the employee so they can carry on paying UK NICs.