Simply put, a CT600, otherwise referred to as a Company Tax Return, is the filing required to pay tax on your earnings. From small businesses to larger corporate firms, this tax payment is required and is referred to as corporation tax.

A CT600 form is part of a Company Tax Return. The form and other supporting documents constitute the Company Tax Return, which must be submitted to HMRC if a company receives a ‘Notice to Deliver a Company Tax Return’. Limited companies use the information in a CT600 form to calculate the Corporation Tax that they owe.

What is CT600 tax return?

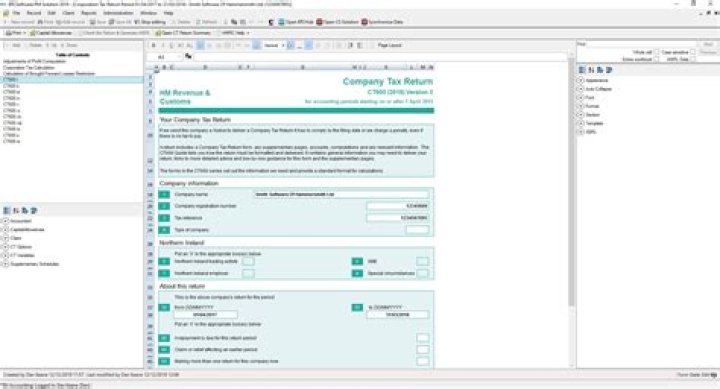

A CT600 form is used by a limited company to file its Company Tax Return to HMRC.

Is a CT600 a tax return?

What is a CT600 Company Tax Return? CT600 Corporation tax form is used to report Company Tax Return. A company tax return is not just the company tax return form CT600 and any supplementary pages but also: Accounts* for the period covered by the return and.

Who needs to complete CT600?

Who should file company tax returns with HMRC. All business have a legal obligation to report annually the financial health of their business to the regulating authority. One of which is you must complete and submit Company Tax Return through Form CT600 with HMRC and pay Corporation Tax on profits from doing business.

When do I need to complete the CT600?

(Practice users) If your accounts cover a period of over 12 months, you’ll need to complete the CT600 for two periods, as follows: Prepare the accounts for the full period and generate an XBRL version. Apportion the profit/loss into a 12-month period and the remaining days – using days meets the HMRC…

How to complete the CT600 corporation tax return?

Follow these steps to input trading and property income on a CT600 form: Enter the figure for Profit/ (loss) on ordinary activities before taxation – this is the total of trading profit/ (loss) and property profit/ (loss). Enter Disallowable expenditure (Depreciation). Go to Tax adjusted… How do I complete the CT600 for a long period of accounts?

How to record franked investment income on CT600?

Franked Investment Income (FII) is the name for UK dividends that a limited company receives from another company. To record FII on a CT600: SimpleSteps: CT600 Core > Trade and Professional income > Tax adjusted profit/ (loss) worksheet – disallowable expenditure. HMRC Forms Mode:… Why can’t I print my document or create a PDF?

How to input trading and property income on a CT600?

Follow these steps to input trading and property income on a CT600 form: Enter the figure for Profit/ (loss) on ordinary activities before taxation – this is the total of trading profit/ (loss) and property profit/ (loss). Enter Disallowable expenditure (Depreciation).