Taxpayers and tax return preparers use this form to disclose items or positions that are not otherwise adequately disclosed on a tax return to avoid certain penalties.

Is as 22 mandatory?

Accounting Standard (AS) 22, ‘Accounting for Taxes on Income’, issued by the Council of the Institute of Chartered Accountants of India, comes into effect in respect of accounting periods commencing on or after 1-4-2001. It is mandatory in nature2 for: (b) All the accounting periods commencing on or after 01.04.

Which is the primary purpose of the income tax rate reconciliation footnote disclosure?

Changes in Tax Law (applicable to all entities) The purpose of this disclosure is to assist users in assessing changes in tax laws that would have an effect on future cash flows.

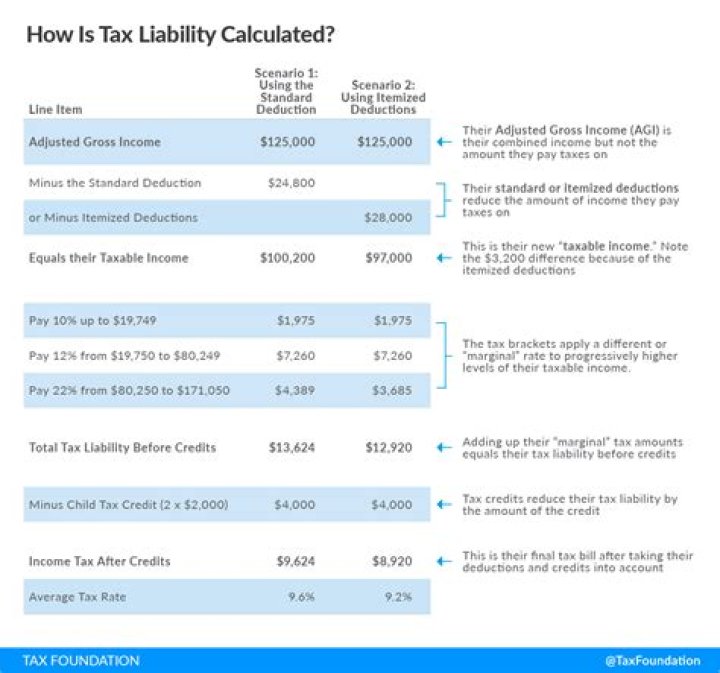

What is taxable income accounting?

Taxable income is the portion of a person’s or company’s gross income that the government deems subject to taxes. Taxable income consists of both earned and unearned income. Taxable income is generally less than adjusted gross income because of deductions that reduce it.

What factors should the company consider in determining the need for a valuation allowance?

Valuation Allowances There are four criteria to consider when deciding whether a VA is needed: Taxable income in carryback years if carryback is permitted. Taxable temporary differences. Future taxable income exclusive of taxable temporary differences.

What sources of income may be relied upon to remove the need for a valuation?

Sources of income that may be relied upon to remove the need for a valuation allowance are: Taxable temporary differences been reversed.

How does a valuation allowance work?

A valuation allowance is a reserve that is used to offset the amount of a deferred tax asset. The amount of the allowance is based on that portion of the tax asset for which it is more likely than not that a tax benefit will not be realized by the reporting entity.

What is not considered taxable income?

What’s not taxable Inheritances, gifts and bequests. Cash rebates on items you purchase from a retailer, manufacturer or dealer. Alimony payments (for divorce decrees finalized after 2018) Child support payments.

Why do we need income computation and disclosure standards?

1. Issue: Need for Income Computation and Disclosure Standards (ICDS) 1.1. The objective of ICDS was to bring greater consistency in the application of accounting principles in computation of taxable income, to simplify the implementation of provisions of the Income Tax Act, 1961 (Act) and to reduce tax disputes. 1.2.

Do you need to know about sample disclosures?

Further, the sample disclosures are not a substitute for understanding reporting requirements or for the exercise of judgment. Entities are presumed to have a thorough understanding of the requirements and should refer to accounting literature and SEC regulations as necessary. 1 ASB Accounting Standards Codification Topic 740, F Income Taxes.

When to disclose impact of new tax law?

After the enactment of a new tax law, registrants should consider disclosing, when material, the anticipated current and future impact of the law on their results of operations, financial position, liquidity, and capital resources.

When to notify CG of income computation and disclosure standards?

It further provides that the Central Government (CG) may notify, from time-to-time, Income Computation & Disclosure Standards (ICDS) to be followed by any class of taxpayers or in respect of any class of income.