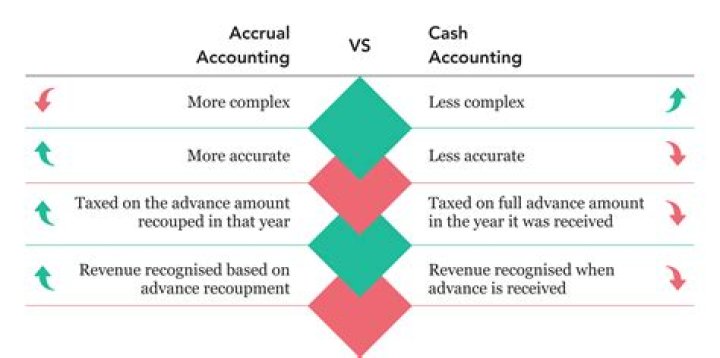

1.3 Cash Accounting Scheme The scheme allows you to account for VAT (output tax) on your sales on the basis of payments you receive, rather than on tax invoices you issue.

Who can use cash accounting for VAT?

Most small businesses are eligible to use the Scheme, as long as your firm is not expected to turnover more than £1.35m over the following 12 months. You can continue using the Scheme until your turnover breaches the £1.6m barrier.

Can you change from standard VAT to cash accounting?

Change your VAT basis to Cash in your financial settings. Run your VAT return for your first period using the cash basis. Compare the VAT Audit report for the current period, with the VAT Audit report from your last VAT period. Look for invoices or bills you’ve already accounted for in the previous VAT return.

When must you leave the cash accounting scheme?

You should leave at the end of a VAT accounting period. You do not have to tell HMRC you’ve stopped using it, but you must report and pay HMRC any outstanding VAT (whether your customers have paid you or not). You can report and pay the outstanding VAT over 6 months.

What is the cash accounting limit?

The cash accounting scheme is aimed at smaller businesses, so in order to be eligible your estimated VATable sales for the next 12 months must be no more than £1.35 million. Once you’ve joined the scheme you can stay on it until your annual VATable sales exceed £1.6 million.

What is the turnover limit for VAT cash accounting?

£1.35 million

To join the scheme your VAT taxable turnover must be £1.35 million or less. Talk to an accountant or tax adviser if you want advice on whether the Cash Accounting Scheme is right for you.

What is the turnover limit for cash accounting?

To use the Cash Accounting VAT Scheme, your business must: Have an estimated VAT taxable turnover of less than £1.35 million.