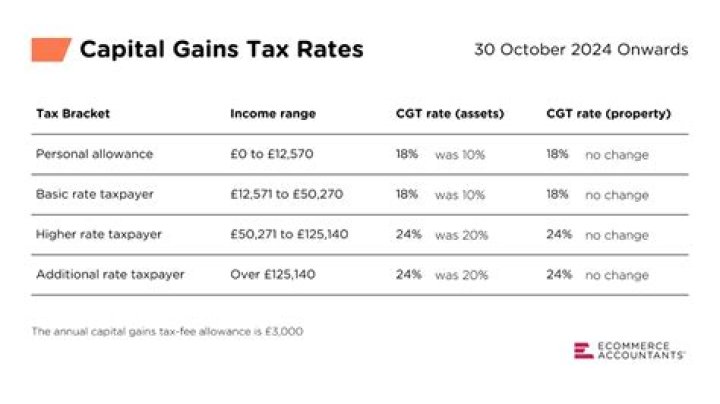

The following Capital Gains Tax rates apply: 10% and 20% tax rates for individuals (not including residential property and carried interest) 18% and 28% tax rates for individuals for residential property and carried interest.

How far back does CGT go?

HMRC’s default time limit of six years after the end of the relevant tax year (for income or capital gains assessments) is extended to 6 years if the loss of tax was brought about carelessly. If the tax loss was deliberate (i.e. fraud), the time limit extends to 20 years.

What happens if I don’t have receipts for capital gains?

If you do not have records You must try to recreate your records if you cannot replace them after they’ve been lost, stolen or destroyed. If you fill in your tax return using recreated records, you’ll need to show where figures are: estimated – that you want HMRC to accept as final.

Do I have to declare CGT?

You must report and pay any tax due on UK residential property using a Capital Gains Tax on UK property account within 30 days of selling it. You may have to pay interest and a penalty if you do not report gains on UK property within 30 days of selling it. Sign in or create a Capital Gains Tax on UK property account.

What counts as improvements for capital gains UK?

You can deduct costs of buying, selling or improving your property from your gain. These include: estate agents’ and solicitors’ fees. costs of improvement works, for example for an extension (normal maintenance costs, such as decorating, do not count)

How do you declare CGT?

Report and pay the tax straightaway You can use the ‘real time’ Capital Gains Tax service immediately if you know what you owe. You need to report your gain by 31 December in the tax year after you made the gain. For example, if you made a gain in the 2020 to 2021 tax year, you need to report it by 31 December 2021.

How long can HMRC chase unpaid tax?

HMRC will investigate further back the more serious they think a case could be. If they suspect deliberate tax evasion, they can investigate as far back as 20 years. More commonly, investigations into careless tax returns can go back 6 years and investigations into innocent errors can go back up to 4 years.