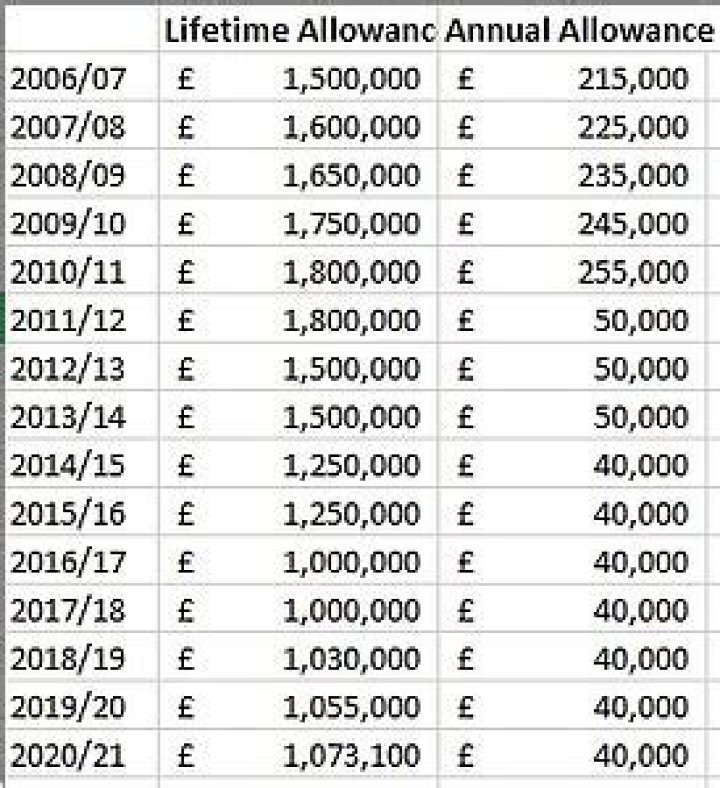

So, effectively, your lifetime allowance determines the amount of benefit you can receive before you have to pay tax on either pension income or lump sums. The current standard lifetime allowance is £1,073,100.

How do I work out my pension lifetime allowance?

To calculate the total pension value for lifetime allowances, for these pensions, there’s a formula. Multiply your expected annual pension by 20 and add this figure to the amount of any tax-free, cash lump sum from that pension.

What is the lifetime allowance for 2021 22?

£1,073,100

of income tax. The lifetime allowance (LTA) for tax year 2021-22 is £1,073,100.

How do I avoid the lifetime allowance charge?

A common strategy is to withdraw tax-free cash from the pension. This leaves fewer funds in the pension to grow, reducing the potential second LTA charge at age 75.

What is the maximum lifetime pension allowance?

Level of protection This gives you a personal lifetime allowance equal to the value of your pensions on 5 April 2016, the day before the lower allowance was introduced – subject to a maximum of £1.25m.

Who pays the lifetime allowance charge on death?

If a lifetime allowance charge is due, the dependant/nominee is liable for it. The scheme administrator will pay the death benefits out without regard to any potential lifetime allowance charge. The lifetime allowance charge will be 55% under BCE 7 and 25% under BCE 5C or 5D.

Does lifetime pension allowance include state pension?

The lifetime allowance is the total value of pension savings you can have before incurring a tax penalty on them. The allowance applies to all the pensions you have, including any defined-benefit (DB) or final-salary schemes, but excluding your state pension.

Is there a lifetime allowance charge on death?

There may be a Lifetime Allowance Charge (a tax charge, where death benefits from pension plans exceed the deceased person’s available Lifetime Allowance), on any excess of the total death benefits from pension plans over the deceased person’s available Lifetime Allowance.

How is pension lifetime allowance calculated?

Is it worth exceeding LTA?

It may be better to pay the 25% lifetime allowance tax charge than the 40% inheritance tax charge. Contributing to a defined benefit pension. These are very valuable pensions and the income you receive from them is normally worth far more than any tax charge that will apply.

How does pension lifetime allowance work?

The lifetime allowance is the limit on how much you can build up in pension benefits over your lifetime while still enjoying the full tax benefits. If you go over the allowance, you’ll generally pay a tax charge on the excess at certain times.

Why is there a pension lifetime allowance?

Is it worth going over pension lifetime allowance?

If the value of all your pension pots exceeds your lifetime allowance you will have to pay the lifetime allowance charge on the excess. The amount of tax you pay depends on how you take the excess. If you take any excess amount above the lifetime allowance as a lump sum it will be taxed at 55 per cent.

How does lifetime pension allowance work?

How is the lifetime allowance applied to pension?

The lifetime allowance represents the amount of money that can be taken from pensions before the lifetime allowance charge applies. The amount of pension benefit is tested against the lifetime allowance at a benefit crystallisation event (BCE). A charge will be applied to any excess over the lifetime allowance.

How can I find out how much lifetime allowance I have?

Ask your pension provider how much of your lifetime allowance you’ve used. If you’re in more than one pension scheme, you must add up what you’ve used in all pension schemes you belong to. What counts towards your allowance depends on the type of pension pot you get.

When was the lifetime allowance reduced in the UK?

The lifetime allowance was reduced in April 2016. You can apply to protect your lifetime allowance from this reduction. Tell your pension provider the type of protection and the protection reference number when you decide to take money from your pension pot.

How much can I take out of my pension if I take a lump sum?

This uses up to 9.3% of the standard lifetime allowance. If you take a £25,000 Uncrystallised Funds Pension Lump Sum (UFPLS) withdrawal, only £25,000 will be tested against your lifetime allowance or 2.32% of the standard lifetime allowance.