Since 1 January 2019, your employer no longer has to give you a form P45 when you leave a job. Instead, they enter your leaving date when submitting details of your final pay and deductions to Revenue. The Department of Employment Affairs and Social Protection no longer require a P45 for claims.

Does a P45 replace a P60?

A P45 is similar to a P60 – the key difference is that you’ll get a P45 when you leave your job. So, a P45 summarises your income and tax payments for the tax year so far (rather than for the whole tax year).

What do I do if I don’t have a P45 or P60?

If your new employee doesn’t have a P45 they should request one, or a copy, from their former employer. In the meantime you should use the data from the starter checklist from your new employee to work out a temporary tax code.

Will my old employer have a copy of my P45?

You cannot get a replacement P45. Instead, your new employer may give you a ‘starter checklist’ or ask you for the relevant details about your finances to send to HM Revenue and Customs ( HMRC ).

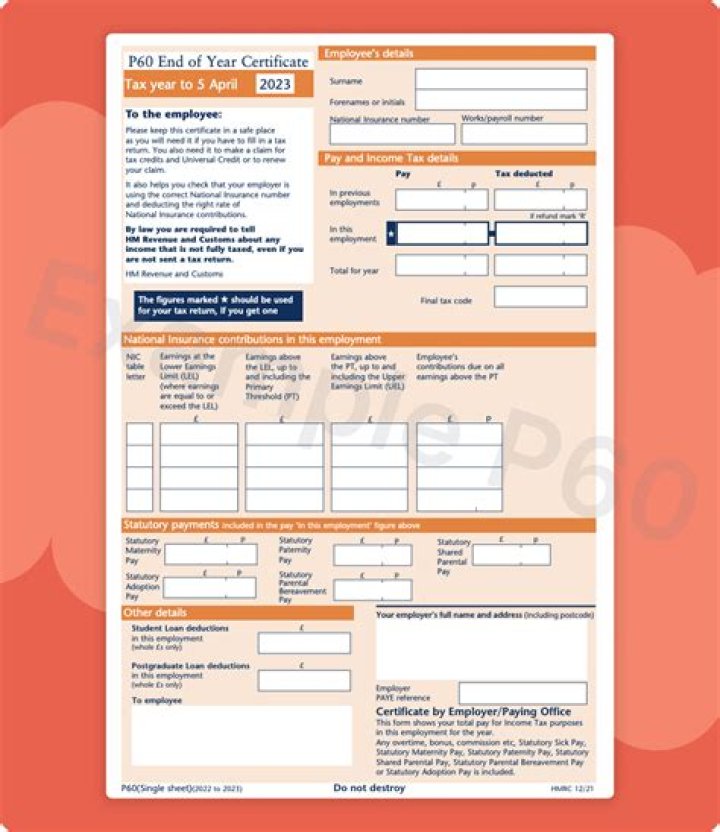

What’s the difference between P60 and P45?

A P60 isn’t given to you when you leave a job. Instead, you get it from your current employer at the end of the UK tax year. A P45 only includes the tax you’ve paid in the tax year up to the point you left a job, but a P60 covers the tax you’ve paid in the entire tax year.

Are employers legally obliged to provide a P45?

Employers are required by law to send P45 Part 1 details to HMRC when an employee leaves their employment. Those not in RTI are required to send the information on form P45 Part 1.

When you start a new job do you need P45 or P60?

When you take on a new employee you’ll need to have a P45 form from their previous employer – the P60 is a year-end summary of their pay, tax and benefits, and won’t give you their correct pay/tax details to date. Their P45 will tell you: The person’s full name. The date they left their last job.