From FY 2020-21, a citizen of India or a person of Indian origin who leaves India for employment outside India during the year will be a resident and ordinarily resident if he stays in India for an aggregate period of 182 days or more.

Who is considered resident of India?

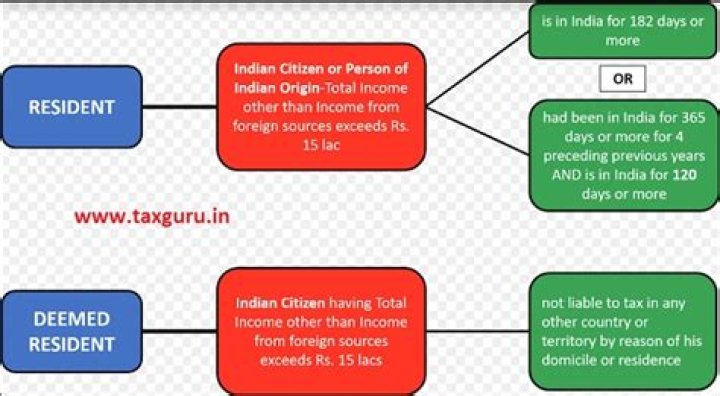

Generally, an individual is said to be resident in India in a fiscal year, if he is in India for more than 182 days in India.

What is the criteria to determine the residential status of individual in India?

An individual is said to be resident in India in any previous year, if He has been in India during the previous year for a total period of 182 days or more OR He has been in India during the 4 years immediately preceding the previous year for a total period of 365 days or more and has been in India for at least 60 days …

Who is resident in India as per income tax Act?

Resident. A resident taxpayer is an individual who satisfies any one of the following conditions: Resides in India for a minimum of 182 days in a year, or. Resided in India for a minimum of 365 days in the immediately preceding four years and for a minimum of 60 days in the current financial year.

Is India a tax resident country?

An Indian citizen having India-sourced taxable income exceeding INR 1.5 million during the relevant tax year will be deemed to be a resident of India if one is not liable to tax in any other country by reason of domicile or residence or any other criteria of similar nature.

How an individual will become resident?

A resident individual will be treated as resident and ordinarily resident in India during the year if he satisfies following conditions: (1) He is resident in India for at least 2 years out of 10 years immediately preceding the relevant year.

Who is RNOR in India?

Resident but Not Ordinary Resident (RNOR) status is given to those people who have been Non-Resident in India during 9 out of 10 financial years preceding that year, or people who have been in India during 7 previous years preceding that year for a period of total 729 days or less.

How can I prove my Indian address?

Indian Address Proof for Passport Renewal In USA

- Any Indian utility bill like electricity, gas, water, landline telephone bill (MTNL/BSNL) bill from the last 3 months. OR.

- Aadhar Card OR.

- Unexpired Indian Drivers license OR.

- Recent Bank Statement from Indian Government bank.

A comes to India on or before 30 September, he will be treated as resident for that tax year. If Mr. B comes to India on or before 31 January and has stayed in India for 365 days or more during the four tax years preceding the relevant tax year, he will be treated as resident for that tax year.

Who is resident in India as per Income Tax Act?

Who is Indian citizen as per income tax?

A person shall be deemed to be of Indian origin if he, or either of his parents or any of his grand-parents, was born in undivided India.

How residential status is determined?

The residential income always determined for the previous year, whose income we are going to tax; 3. Residential Status of persons should be determined each year, since it may be possible that his/its residential status may be change in next previous year; 4.

What makes an Indian citizen a resident of India?

How is residency determined for tax purposes in India?

For individual, tax residency is decided on the basis of number of days stayed in India. Generally, an individual is said to be resident in India in a fiscal year, if he is in India for more than 182 days in India. The relevant section is Section 6 of the Income Tax Act,1961 to determine residency in India. In case of any doubt, please refer to.

When do you become a non resident of India?

–If he/ she is in India for at least 365 days during preceding 4 years AND at least 60 days in that previous year. So if any of these conditions are not satisfied then the person will be considered as NON-RESIDENT INDIAN for income Tax purposes.

How long do you have to be resident in India to file tax return?

Generally, an individual is said to be resident in India in a fiscal year, if he is in India for more than 182 days in India. The relevant section is Section 6of the Income Tax Act,1961 to determine residency in India. In case of any doubt, please refer to